You might’ve heard the doom and gloom around AI taking all of our jobs. But chances are, if you can hold a conversation, you’re still miles ahead of the AI game. Afterall, who’s going to blab with subbies or builders about what they got up to over the weekend?

At this stage, what AI is great at is doing the tedious and time-consuming jobs we don’t want to do; the boring stuff that’s probably better left for computers. So let’s set the record straight. AI isn’t here to kick us out of the workforce, it’s more like the ultimate wingman, helping us work smarter, not harder.

In the construction industry, where one little slip-up can cost big time, AI can swoop in and cut down on human errors in things like estimates and takeoffs. That means fewer redos and smoother sailing all around.

As AI keeps evolving, the whole construction game speeds up – we can leave the competition in the dust and zoom ahead. But let’s dive a bit deeper. AI isn’t just about making our jobs easier—it’s about unleashing our full potential. Imagine having a virtual assistant who knows exactly what you need, when you need it. That’s the power of AI. It’s like having a personal coach cheering you on every step of the way.

And here’s the kicker: AI isn’t just for the big players. Businesses of all sizes can get in on the action too. So, whether you’re a seasoned pro or just starting out, AI has something to offer everyone. It’s not about replacing humans; it’s about empowering them.

At EstimateOne, we have two major ways we incorporate AI:

- Superseding addendums

When you upload documents for addenda into EstimateOne, we’ll look at the file names, find similarities and suggest which documents you should supersede

- Finding relevant projects

Every project that enters EstimateOne is scanned for keywords. That way, whenever one of your saved keywords is mentioned in a document, we’ll let you know

Interested in learning more? Get in touch for a demo!

Look, it’s no secret that the construction industry is traditionally male dominated. While there’s been strides of change, a reduction of the gender pay gap from 16% to 7% (as per latest figures), there’s still a way to go. This International Women’s Day serves as a powerful reminder of the strides we’ve made towards gender equality and the work that still lies ahead. In the construction industry, historically dominated by men, the journey towards inclusivity and diversity is tough. At EstimateOne, we’re committed to not just discussing inclusion, but actively embodying it, as highlighted by Zaiga Finnis, our Chief Customer and Commercial Officer:

“In my journey navigating the construction industry from interior designer to my current role at E1, I’ve seen first-hand the importance of supportive workplace communities that empower women. Building networks, seeking mentors and career sponsors, and staying updated on industry activities are crucial for career progression.

It’s vital to offer professional development, mentoring, and opportunities to foster inclusivity for all. With 50% of our senior leadership team and executives being women, we’re not just talking about inclusion, we’re living it.”

Zaiga’s experience stresses the importance of creating environments where women can thrive. At EstimateOne, we understand that empowering women goes beyond hiring; it’s about nurturing their growth, ensuring they have access to the same opportunities as their male counterparts, and recognising their contributions to our industry’s innovation and success.

Let’s use this International Women’s Day to celebrate the achievements of women in construction while acknowledging the road ahead. Together, we can challenge stereotypes, fight bias, and broaden perceptions. Join us in building a construction industry where everyone, regardless of gender, can construct a successful and fulfilling career.

MTM Construction, a leading Building and Civil Engineering firm in Scotland, has improved its operations big time by moving away from outdated, paper-based methods and instead, implementing EstimateOne.

This change in their estimating processes has generated a 75% reduction in time, cost savings, and improved industry networking. Previously bogged down by manual spreadsheets and communication methods, MTM’s adoption of EstimateOne has streamlined project management, allowing for easy document sharing, inquiries, and quotations in one centralised location.

Steven Lyons, an Estimator at MTM, highlights how tiring the previous methods were, including the laborious task of managing email groups for tender requests—a challenge that EstimateOne has effectively addressed. The platform’s introduction has not only drastically improved the tendering process but also boosted teamwork and made it easier for everyone to get the info they need, without doing the same stuff over and over.

Lyons credits EstimateOne for giving them a leg up in the competition, pointing out the benefits of having all subcontractor info in one spot and being able to get bids out faster. This smooth operation means they don’t have to hire more people, saving them money. Simon Herod, International Lead at EstimateOne, echoes that using old-school methods for estimates is a broader industry challenge and that going digital can really change the game.

Despite being labelled as fiddly and time-consuming, trade packages are a necessary evil in the world of construction and contracting. The reason behind employing trade packages goes beyond just paperwork; it’s a strategic move to support subcontractors and optimise the tendering process. Here, we will explore the significance of trade packages, the motivation behind them, and practical steps to streamline the entire process.

The fiddly nature of trade packages

Do you spend hours dragging document after document into folder after folder? Trade packages often involve details, specifications, and requirements that demand meticulous attention. From material lists to project timelines, every aspect needs to be carefully documented. This precise nature can make trade packages seem fiddly and time-consuming. However, it’s essential to recognise the role they play in ensuring project efficiency, cost-effectiveness, and overall success.

Supporting subcontractors and enhancing quoting

The primary motivation behind engaging in trade packages is to support your subbies. By providing comprehensive and organised information, you can empower subbies to understand project requirements better. You know the phrase ‘you scratch my back, I’ll scratch yours’? Well that comes to mind here, as subbies are scratching your back when they shoot you off a quote (no ones getting paid yet). So the least we can do is make their quoting life easier. Ultimately, this benefits both parties, and leads to successful project outcomes.

Streamlining the trade package process

While trade packages may seem daunting, getting your bits and bobs in order early can save you a lot of headaches down the track. Here are some strategies:

1. Label, label, label:

Clear and consistent labelling is crucial for easy navigation through trade packages. Get your team on a naming system and stick with it. Consistency is key.

2. Break into sub-categories:

Categorising trade packages into sub-sections based on specific criteria can simplify the process. This allows for better organisation and quicker reference when needed.

3. Utilise software solutions:

It would be remiss of us if we didn’t get a cheeky plug in here. Using software tools, like the EstimateOne doc matrix and its various shortcuts, can significantly streamline the trade package process. These tools are designed to enhance efficiency, reduce errors, and save valuable time.

By recognising the role trade packages play in supporting subcontractors and optimising the quoting process, main contractors can approach them with a strategic mindset. Implementing efficient labelling and sub-categorisation, and utilising specialised software like EstimateOne helps to turn this mundane task into a well-organised and manageable aspect of your role and business.

The adage, “those who do not learn from history are doomed to repeat it,” holds true in the world of construction and commercial estimation. Each completed project offers a goldmine of insights, shedding light on where estimations hit the mark and where they veered off course. Conducting a thorough review of past project estimations isn’t just a best practice—it’s an essential one. Here’s a structured approach to ensure your reviews are both efficient and effective.

1. Set clear objectives for the review

Before diving into the numbers, outline what you aim to achieve. Are you looking to improve accuracy, speed up the estimation process, or reduce contingencies? Pinpointing your objectives will guide the review process.

2. Gather all relevant data

This is the foundation of your review. Collect data on original estimates, final project costs, changes to the scope and the associated cost implications, and any unexpected costs that arose.

3. Assemble a diverse review team

Your review team should consist of various stakeholders to ensure all perspectives are considered, enriching the quality of the review. Stakeholders could include; the original estimator(s), project managers, site supervisors, finance personnel, and supply chain representatives.

4. Segment the review

Break down the project into its various components, including labour, materials, equipment, subcontractors, soft costs (permits, insurance, etc.). Reviewing segment by segment will make discrepancies easier to spot and will allow for a more granulated analysis.

5. Identify variances

For each segment, compare the estimated costs to the actual costs. Calculate the variances both in absolute terms and as a percentage. This will highlight areas needing the most attention in future estimations.

6. Understand the why

Numbers tell a story, but they often need interpretation. For each variance identified, delve into the reasons behind it, for example:

- Were there unforeseen challenges on site?

- Did material prices spike unexpectedly?

- Was there an error in the initial estimation?

- Getting to the root cause is crucial for future improvements.

7. Document lessons learned

As insights emerge, document them. Capture both the quantitative data (exact variances and their values) and the qualitative insights (reasons behind the variances, suggestions from the review team).

8. Recommend process improvements

Based on the lessons learned, suggest improvements for future estimations, such as the need for better forecasting tools for material costs, whether there should be a larger contingency for certain types of projects, or whether there is a need for ongoing training in certain areas.

9. Implement feedback loops

To ensure continuous improvement, create a feedback mechanism where the insights from the review are regularly fed back into the estimation process.

10. Regularise the review process

Don’t wait for a project to go significantly over budget to conduct a review. Make it a standard practice to review all projects, regardless of their perceived success or failure. This regularity will instill a culture of continuous learning and improvement.

While the initial goal of commercial estimation is accuracy, no estimator can predict the future with complete certainty. However, by diligently reviewing past projects and embracing a mindset of continuous improvement, estimators can come remarkably close. Remember, every project, whether it sticks to its budget or not, offers valuable lessons. The key is to harness them effectively.

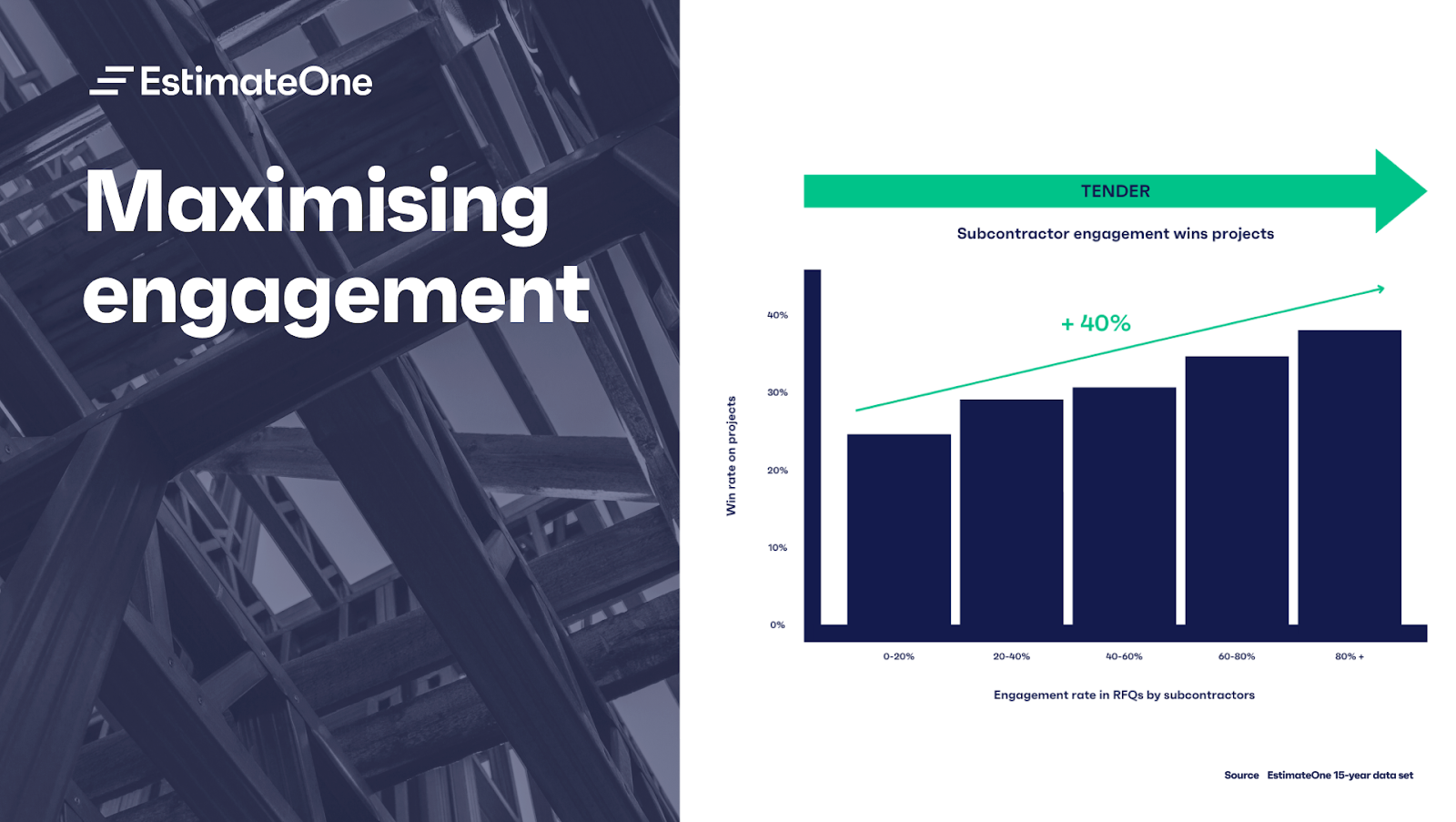

In today’s competitive construction industry, the role of estimators holds huge significance, influencing approximately 80% of a project’s margin even before the actual construction begins. Estimators face daunting challenges due to a tight labor market, persistent supply chain issues, and a high rate of insolvency among construction companies.

Estimators as risk navigators

Estimators and their teams are tasked with navigating these risks. Poor estimation processes can jeopardize business sustainability by either leading to unsuccessful tenders or a surplus of tenders with unsustainable margins. Additionally, making poor subcontractor selections, whether through subpar quotes or partnering with underqualified parties, can result in costly defects down the line. Estimators are on the front lines of managing these challenges, and addressing them head-on can set a business apart from the competition.

Leveraging data for success

To succeed in this environment, businesses must harness data and engagement. At EstimateOne, we’ve collected data that highlights the correlation between higher engagement rates and increased tender success.

But how do you improve engagement?

- Assess your contact network: Your contact book likely contains numerous trades and businesses. Analysing your historic quote coverage by trade and contacts within each trade helps identify areas where you may be lacking. This enables better prioritisation of follow-ups and ensures consistent trade coverage during the limited tender period.

- Optimise your tender process: Gathering quotes is just half the battle. How you handle the tender process is equally crucial. Being selective with RFQs and tailoring them to your specific needs is essential. Creating trade packages, inviting suitable subcontractors, and providing clear communication are all key to long-term success.

- Give feedback: Subcontractors who quote but receive no feedback are likely to lose interest quickly. Providing constructive feedback not only improves their quoting but also encourages them to continue working with your business.

Expanding your subbie network

The data suggest that subbie supply chains have dwindled over the past few years. To overcome this challenge, consider two key strategies:

- Publicly market tenders: Opening your tenders to a wider audience, particularly for projects in new areas or sectors, can help you discover new subcontractors who are genuinely interested in quoting.

- Actively target qualified leads: Use data-driven insights to identify areas where your coverage is lacking and actively target trades that can fill these gaps. Subcontractor directories, like those offered by EstimateOne, can provide a head start in this regard.

Evaluating past performance

One of the best ways to anticipate future performance is by evaluating past performance. For new subcontractors, it’s essential to assess their qualifications and project history. With your existing network, you have the opportunity to not only choose the most qualified subcontractors but also those known for their quality and support, fostering repeat quotes and a smoother procurement stage.

As the industry faces unprecedented challenges – challenges that are unlikely to lessen at any point in the foreseeable future – businesses that prioritise the role of estimators are likely to stand out from the competition and thrive in this evolving landscape.

EstimateOne drastically streamlines the processes of tendering and building subcontractor networks. To get an in-depth look at EstimateOne, book a demo today.

As I’m sure we all know, construction firms have a tiny ~5% profitability margin. With such little room for error, the accuracy of estimating is more important than ever. This is even more crucial given 80% of margins are locked in pre-construction.

When it comes to locking down projects, we don’t tend to focus on the significance of locking down the RIGHT projects. Estimators are the gatekeepers to securing the right projects, but they’re continually grappling with outdated and manual systems.

Often, estimators have to base tenders on subbie quotes from outdated Excel spreadsheets, adding an extra burden to the already risky and tedious task they have on their plates. With only 3% of construction firms using digital technology on at least half of their projects (source), transitioning to digital methods can be a major competitive advantage.

Is it the lack of awareness around these digital solutions that’s holding companies back? Allow us to enlighten you…

A digital process leads to more effective and efficient estimating. That’s not to say manual processes don’t work, just that there’s far better ways to achieve a more accurate and less risky outcome, leading to better decision-making.

And back to our undervalued estimator… digitising their processes enhances project planning, improves visibility across projects and progress, and helps with cost saving. Estimators will be able to nurture existing and foster new relationships with subbies, ensuring all participants in the tendering process are on a shared path. This doesn’t only help the estimators, main contractors, and subcontractors, but it helps the construction industry as a whole, thanks to the reduction of labour shortages that can result.

Embracing the digital era for estimators will spearhead them to a position of greater knowledge, through real-time data and market insights. Allowing them to better navigate supply chain challenges will benefit the industry through more accurate estimates, competitive bidding and improved collaboration across the supply chain.

Death, taxes, and unnecessary stress during the procurement process. For CA’s in the commercial construction industry, these are all certainties of life. And look, things are often out of our control, but to make procurement time more predictable (and less draining), start by streamlining your subbie relationship management.

Here are our top tips for using EstimateOne, and the RFQ connect product to make sure you’re keeping your subbies on side:

- Avoid inundating subbies with generic invitations

A quick way to get a subbie to ‘ghost’ you is by expecting them to shift through a full set of documents when only a few are relevant to them – that’s a one-way ticket to being ignored. EstimateOne lets you send tailored invites and project details to the right subbies. No more spamming them with a ton of stuff. It’s all about real connections with the perfect subbies for your gigs.

- Use data to make decisions

You know what’s key? Data. It’s like your secret weapon for picking the right subbies. Check out subbies’ past projects and performance, see their proven track record, and reduce the risk of projects steering off track.

- Keep subbies well-informed

We always go that little bit further when we feel loved, and subbies are no different. When they feel important and valued, their teamwork and cooperation really shine. EstimateOne keeps the conversation going with subbies. They’ll get project updates without you having to lift a finger, and we’re all about sending them a heads-up, even if a project doesn’t land their way. Remember, subbies find any feedback from builders highly valuable.

- Nurture subbie relationships

Having both pre and post-award teams using the same subbie address book is like a teamwork hack – it just makes things smoother. If a subbie keeps quoting for your estimating team, but never actually wins a contract – there’s a big chance your estimating team will soon lose a key contact. When the teams are able to see the whole picture, it gives delivery a chance to reward those subbies who helped you during tender time. When your whole crew is on the same page, you naturally get to connect better with the subbies who typically come to the table.

Want to get an in-depth look at EstimateOne and RFQ connect? Book a demo today.

As Australia’s leading tender platform, we thought we’d start 2021 by looking back at how the Australian construction industry tendered in 2020.

It’s fair to say that 2020 didn’t pan out as expected. At the start of the year, no one could predict the changes we would eventually make to the way we work, the way we socialise and essentially, the way we live.

Although a global pandemic threw the mother of all spanners in the works – as a whole, Australia and the Australian construction industry managed to steer a steady ship throughout the year.

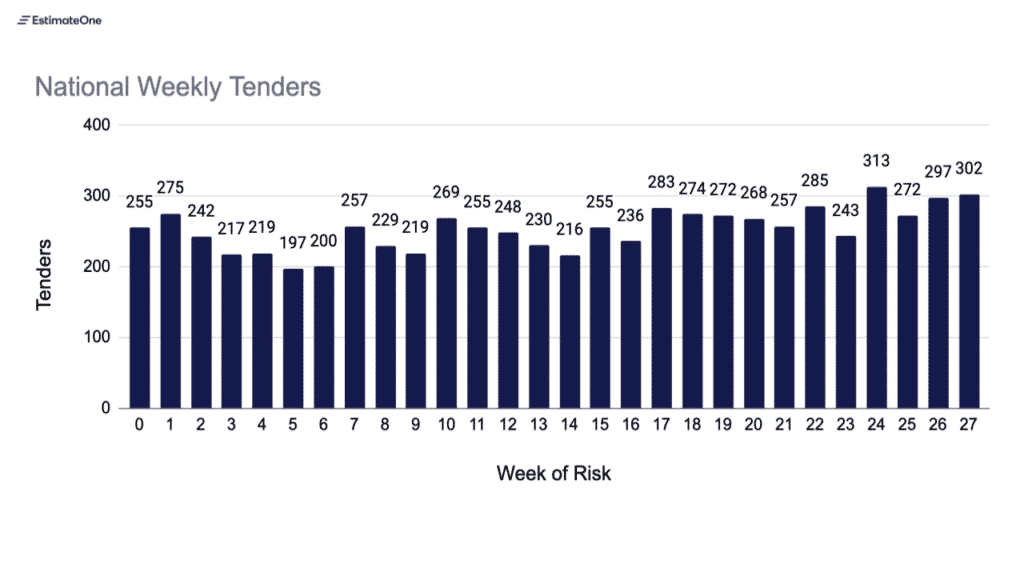

While it’s always great to see a lift in tender numbers, a survey we commissioned mid last year told us that the year wasn’t always smooth sailing.

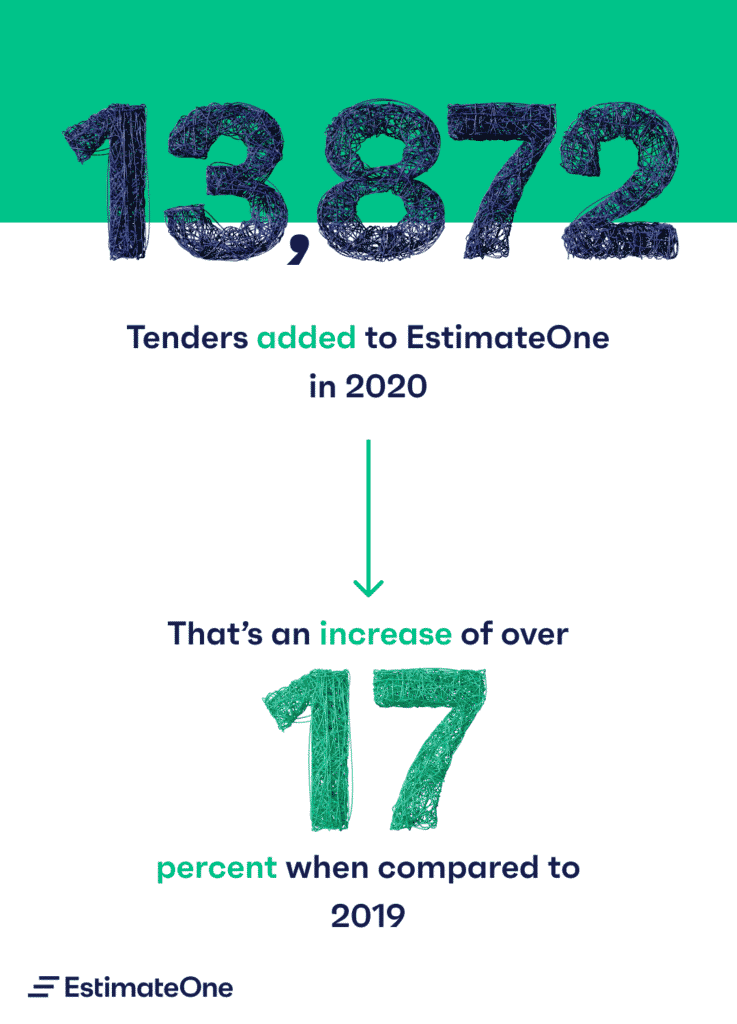

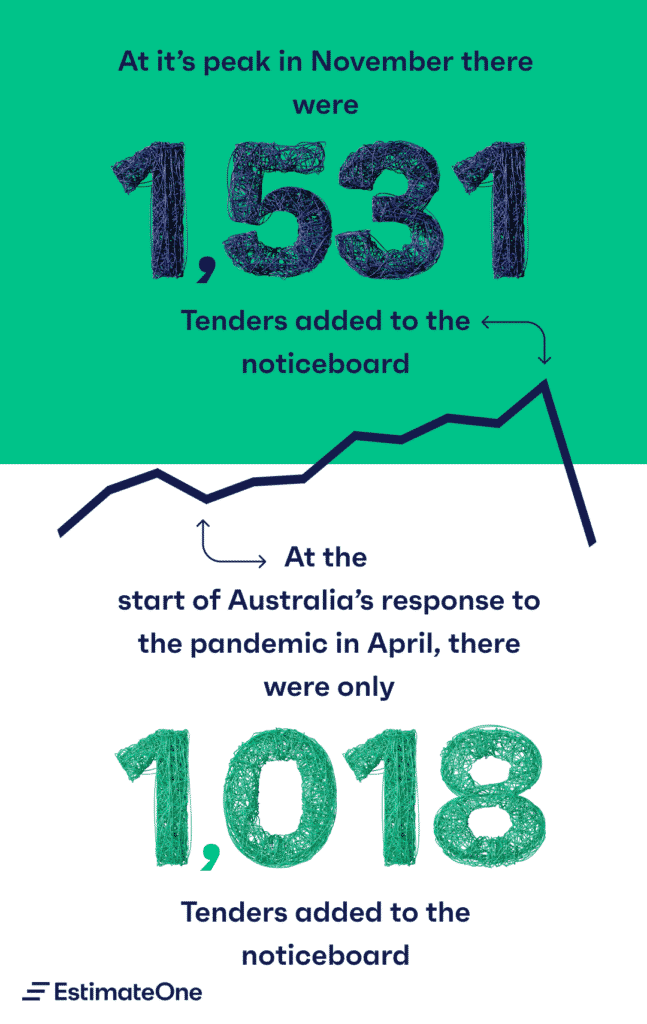

As we can see in the graph above, tendering dipped and continued to stay low around March – June. However, in the back half of the year where tendering made a strong recovery.

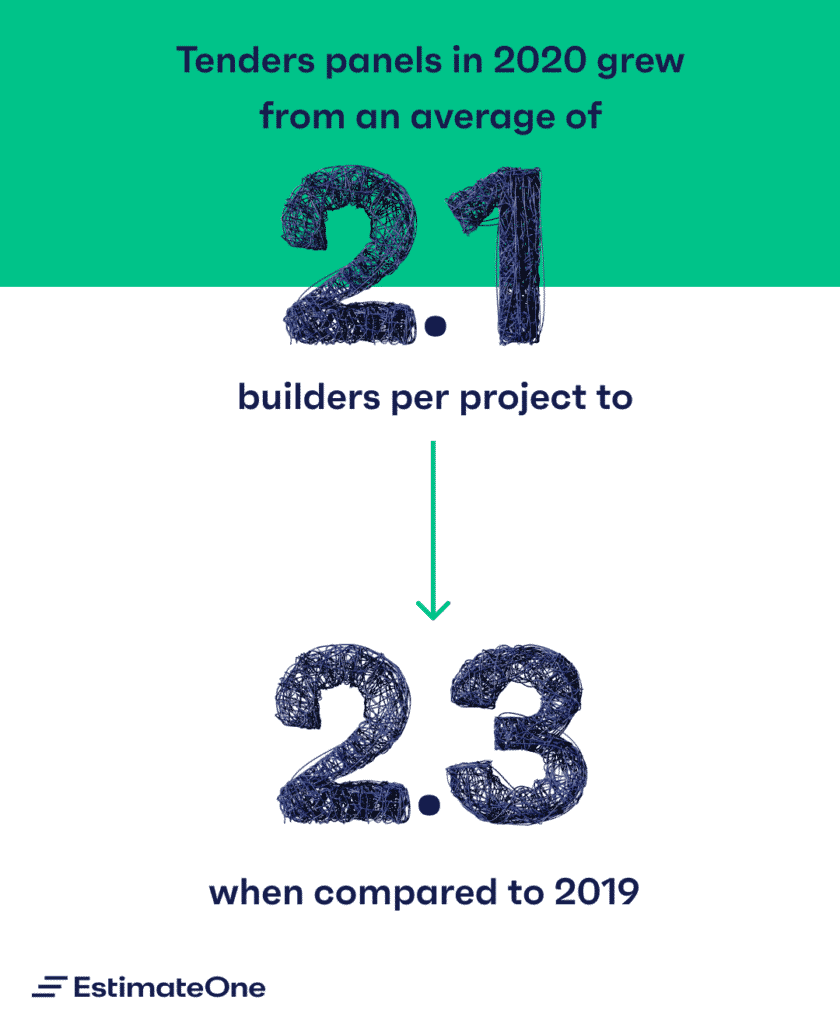

In 2020 we saw an increase in projects added to the noticeboard across all categories. Along with this increase in tendering, we also saw an increase in competitiveness. Compared to 2019, tender panels tended to have more builders.

Anecdotally, we were hearing that market uncertainty was leading to increased competition. Builders were seen to have tendered on jobs that they wouldn’t have usually tendered on in order to sure up a pipeline of work.

If you’re not on already, we’d recommend creating a free EstimateOne account. It’s the best place to access and quote on upcoming construction projects in Australia.

It has been over a month since Premier Andrews announced stage 4 restrictions for Melbourne. While the state as a whole has had to adapt to unprecedented living conditions, the commercial construction industry has had to confront arguably it’s biggest disruption.

On site, progress has slowed as sites are forced to operate at 25% capacity. Off site, current market conditions and an uncertain outlook are continuing to effect tendering and procurement in the industry.

Now that the dust has settled on the initial announcement, we felt it was a good time to provide the industry with an update on what our data is showing us.

What we’re seeing:

Section 1: Tender numbers

Graph 1: National Tender numbers:

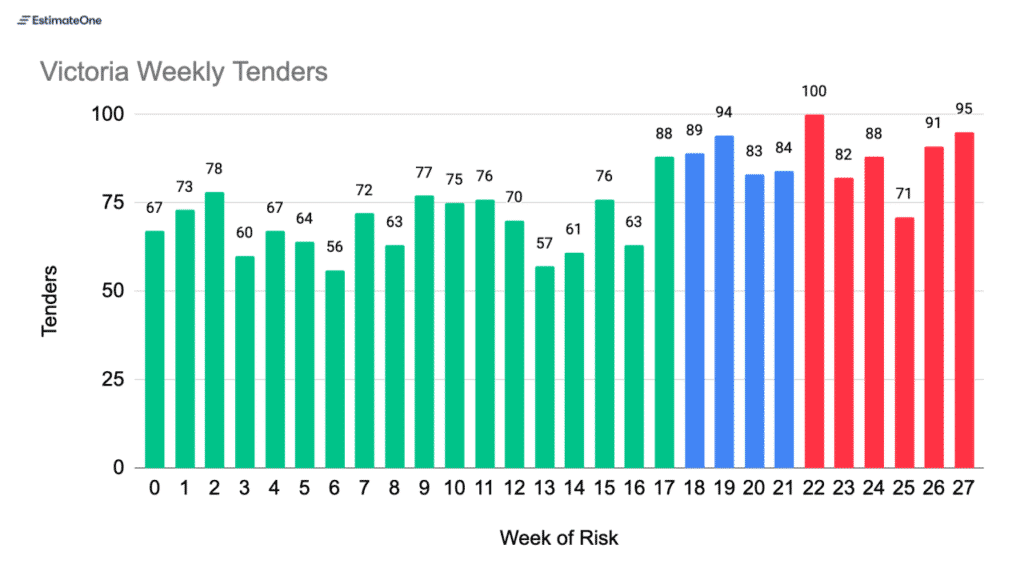

Graph 2: Tender numbers in Victoria:

[Note the blue bars represent stage 3 restrictions and the red represent stage 4]

Analysis:

- While Victoria implemented two additional stages of tighter lockdown restrictions, the number of tenders added to EstimateOne increased when compared to pre-lockdown times

- With Estimating being one of the few departments that can work remotely, this isn’t entirely surprising.

- However, the projects that are going out to tender now have likely been in the pipeline since the start of the year. While these numbers may paint a positive picture, the full effect of COVID-19 will likely be delayed until the full economic impact of the pandemic becomes clearer.

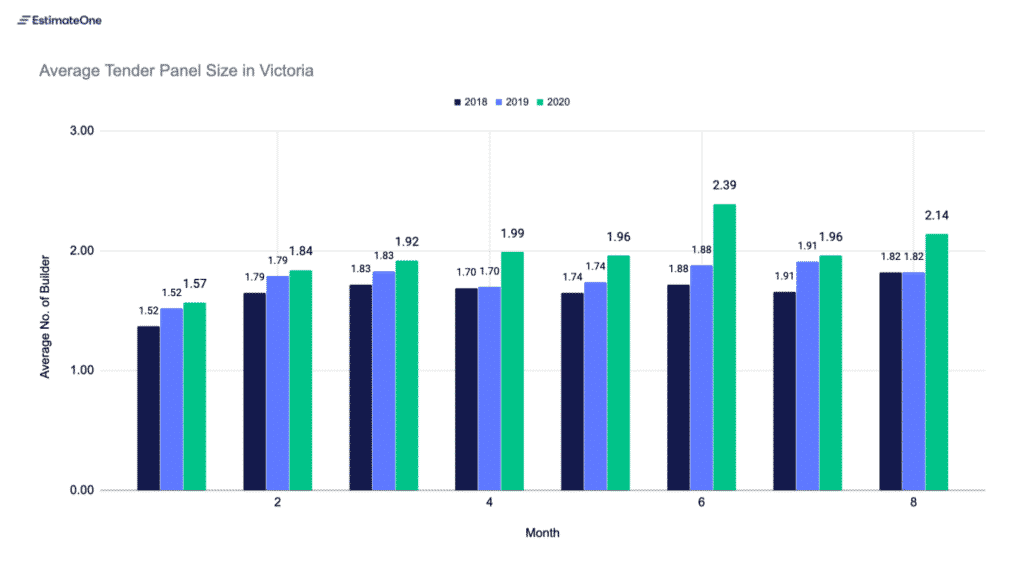

Graph 3: Average tender panel size

Analysis:

- Since the first raft of lockdown measures were introduced in April, tender panels in Victoria have consistently been more competitive when compared to the same time last year.

- Anecdotally we are hearing of builders tendering more, and tendering outside of their usual zone. A previous newsletter we sent out covered this topic [link]

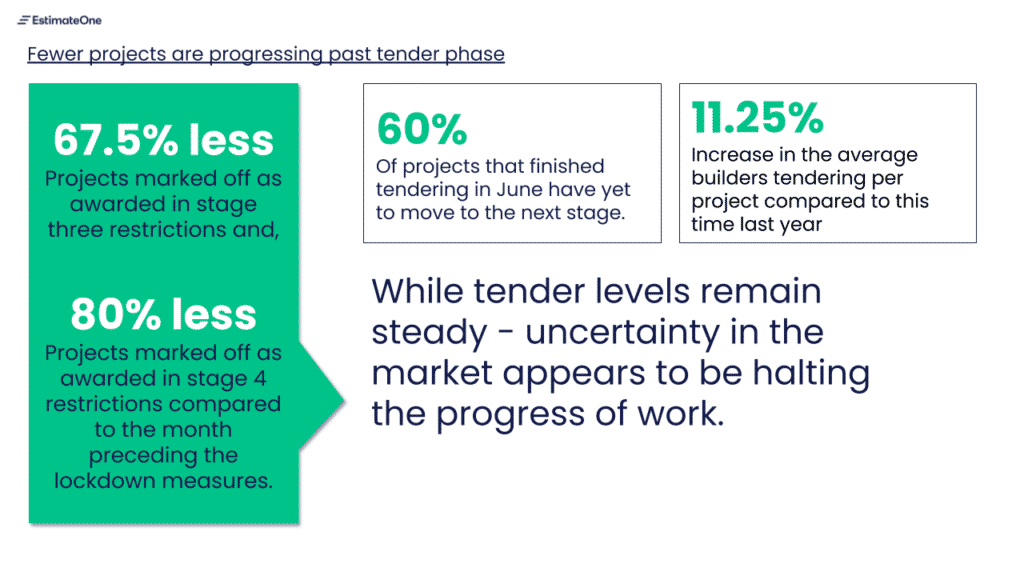

Infographic 1: projects not moving past tender phase

Analysis:

- There has been a steady decline in projects being marked off as awarded since the reintroduction of stage 3 restrictions at the start of July.

- Anecdotally we are being told of an increasing number of projects not getting to the awarded contract stage. We can see this on our noticeboard with 60% of the tenders that closed in June are yet to have anyone on the tender panel mark it off as either won or lost.

- With uncertainty around the market and the potential of further lockdowns, it appears clients are hesitant to agree to a price and commit to spending capital.

What we’re hearing:

Initially, the new rules lead to widespread confusion:

- On the day the initial restrictions were announced, one subbie we spoke to spent three hours on hold to the COVID hotline for business enquiries, only to have his question remain unanswered. It took a further two weeks before his trade was classified as a specialist trade. As he awaited clarification he was effectively unable to conduct business.

- We also heard from a number of head contractors expressing their confusion around the ‘1 site per subbie’ and 25% capacity rules. It was a number of days before the ‘1 site per subbie’ rule was amended so that subbies in specialist trades were able to responsibly move across sites.

Tenders are up, but they aren’t progressing:

- Much like our data suggested, many of the builders we spoke to talked about a number of projects they’re tendering being delayed.

- One builder told us of a few government jobs that have yet to be awarded, speculating that they are nervous to pull the trigger in case further outbreaks / lockdowns delay progress mid-build.

- We have also heard of a site being told to stop mid build as the client wanted to shore up further finance through more pre-sales.

- In a previous newsletter [link], we discussed that while State Governments are fast-tracking projects through the planning phase, the reality is that practically none of these projects have commited finance due to uncertainty in the market. Without finance they won’t be progressing to the construction phase.

This lack of progress is driving market competitiveness.

- Despite a lack of guaranteed finance from early sales – one builder we spoke to believes that developers are pushing ahead trying to take advantage of what they perceive to be a desperate and competitive market. However, without this finance they are unable to pull the trigger and award a contract. This is likely a contributing factor to what we are seeing in our data.

- Head contractors have told us of a more competitive subcontractor market. One builder spoke of a 5% decrease in subcontractor pricing across the board.

- One of the subbies we spoke to told us he’s never quoted more projects, and he’s never quoted tighter margins. This is due to an increase in RFQ’s being received and a need to lock in a future pipeline of work.

- We are also hearing of builders tendering more – one builder told us that while they are winning a similar amount of contracts as they were pre-COVID, this is only a result of them doubling their tendering efforts.

As always, we appreciate the help we get from those who speak with us. If you are seeing anything or have a story to tell, please get in touch so we can help further inform the industry.