COVID-19 Industry Impact Newsletter – 15th of April

It’s hard to believe the pace with which COVID-19 has spread across the world, and the pace with which authorities and societies have reacted to it. From our vantage point at EstimateOne, although cases and restrictions in Australia have increased since our last newsletter, the initial panic seems to be subsiding.

Efforts across the country to ‘flatten the curve’ appear, for now, to be working. The rate of new cases identified is dropping and health systems remain able to handle the volume of patients presenting with the virus.

The Prime Minister has reaffirmed an intention between his office and the State Premiers’ to keep construction sites running, and this is reflected in continued activity across the industry. Tenders are still flowing, projects are still being awarded and construction sites are continuing to operate; although on all fronts we see the impact of COVID-19.

Below we share some more detailed observations to help you navigate the impacts to our industry.

What we’re seeing:

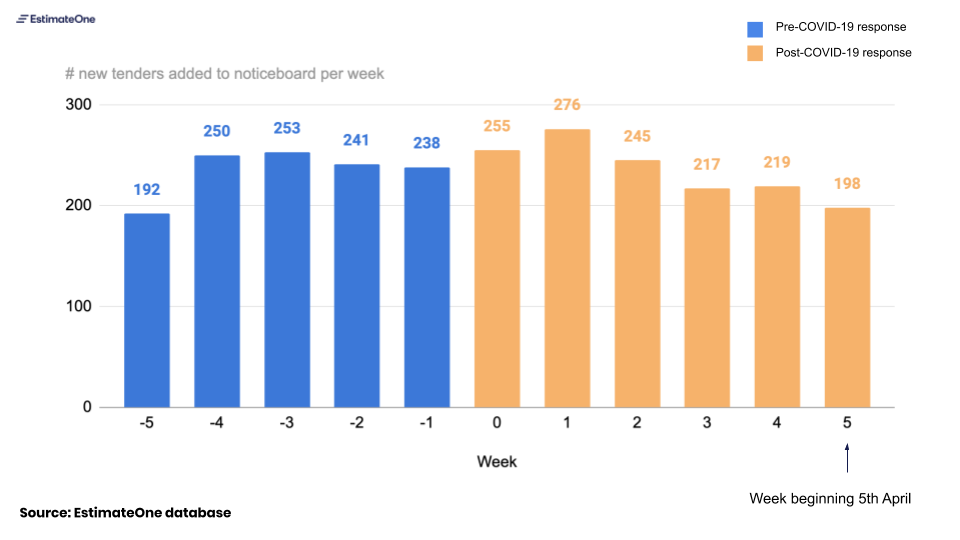

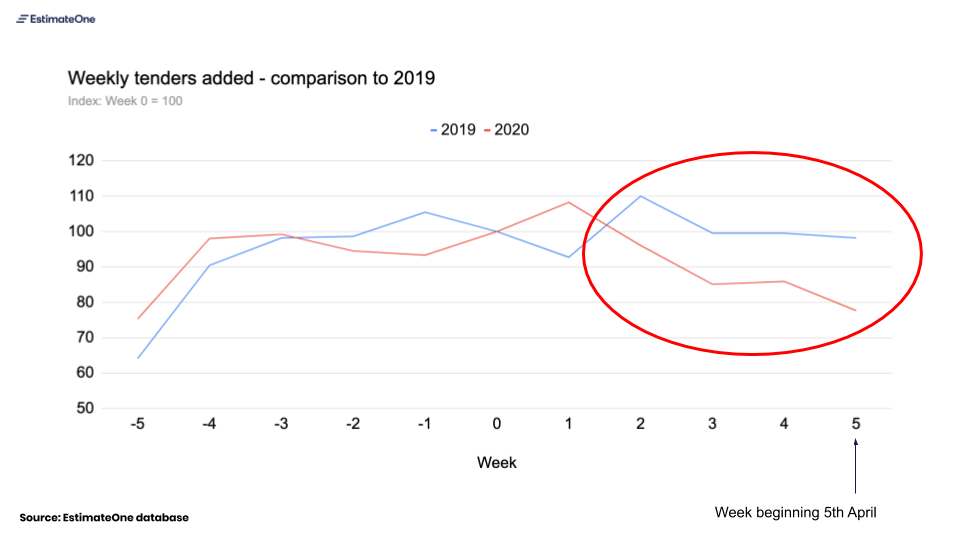

Section 1: Aggregate new tender volumes

Commentary:

Tender volumes dropped from around 250 per week to around 220 in Week 3 of the crisis and this most recent week we saw a further drop to 198 – though a shorter week with Good Friday explains this further fall. We expect this coming week, also shorter, to show lower volumes too.

We have confidence in attributing the March slow down to COVID-19. Last year weekly volumes in March were equal to February numbers, this year they’re ~10-15% down (see chart below)

Section 2: Breakdown by sector

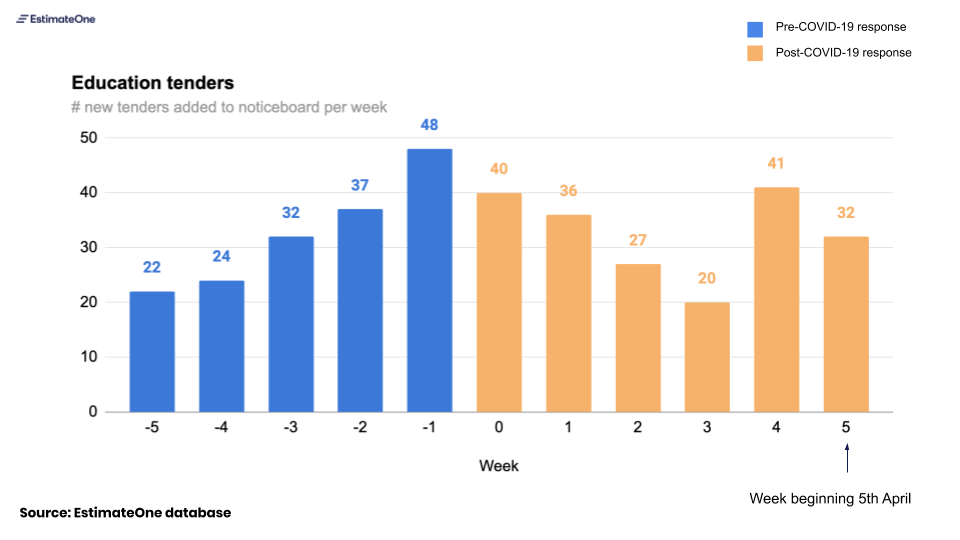

Education:

In the first few weeks of March, education tenders halved from a high point in late February, but the last two weeks have seen an increase. Clients have mentioned education projects in Government pipelines being fast-tracked to tender as a COVID-19 response which may explain this uptick.

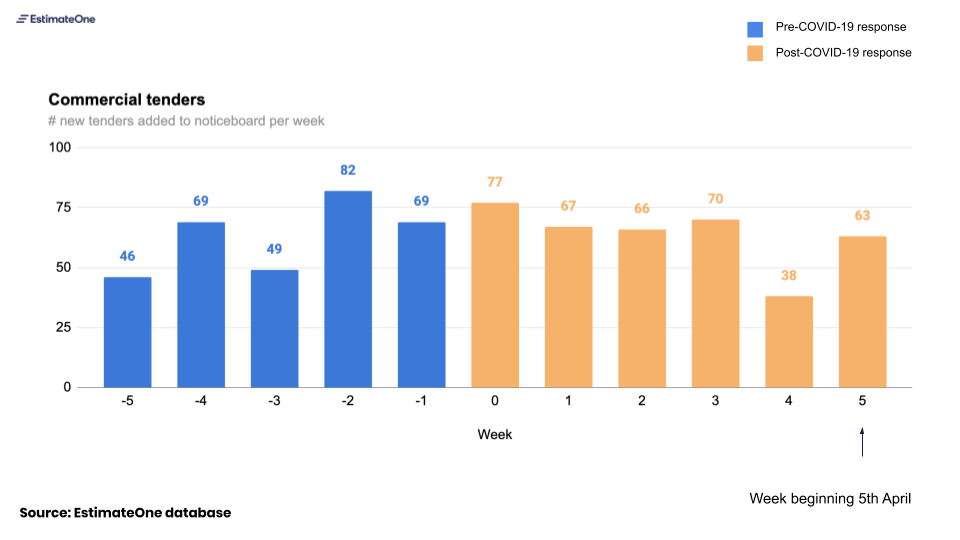

Commercial:

Commercial had a more moderate drop-off which was concentrated in tenders above $2m (lower price tenders saw a reduction in the early weeks of the crisis but have since rebounded)

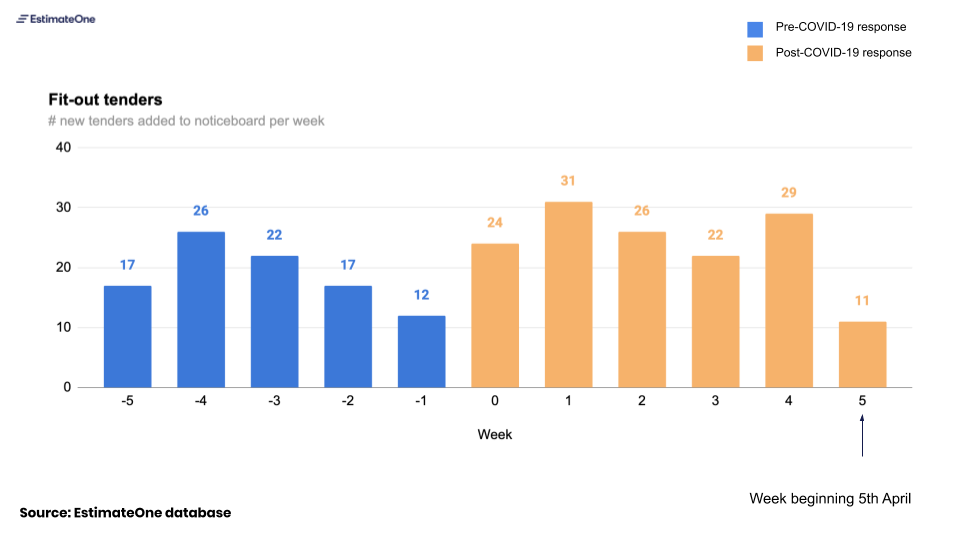

Fitout:

We anticipated fit-out tenders to be amongst those most affected by the crisis and by the lock downs – but volumes remained higher until this last week where we saw a significant reduction. Our builder clients have suggested that their clients have been seeing opportunities to bring forward smaller projects given their empty offices – this is supported by our data; projects under $2m have actually increased since Week 0. (beginning of March)

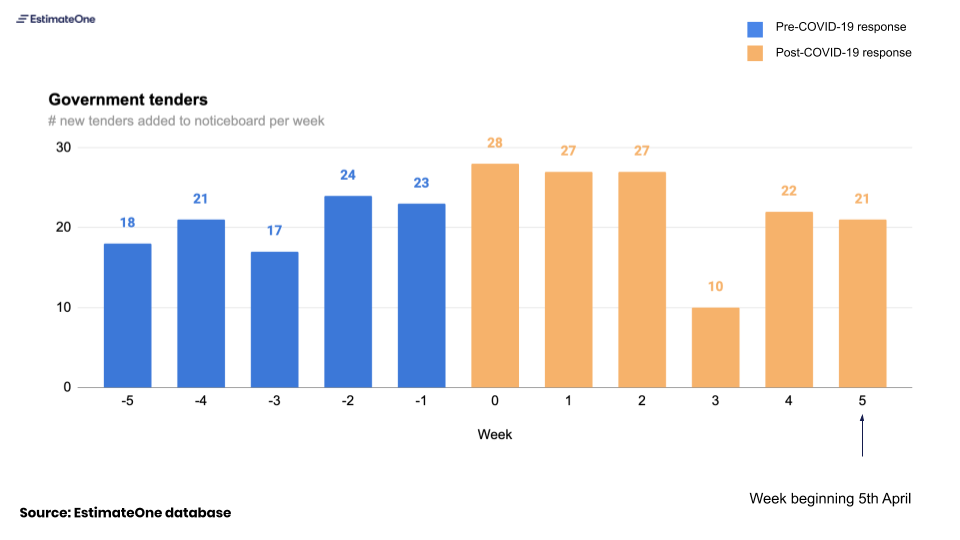

Government:

New government tenders have seen the most significant drop-off amongst sectors (note that this Category excludes tenders categorised to other sectors like Education or Medical which are likely to include Government clients). This drop-off is accounted for largely by a reduction in small tenders $0-$2m, with tender volumes $2m+ holding steady through February and March.

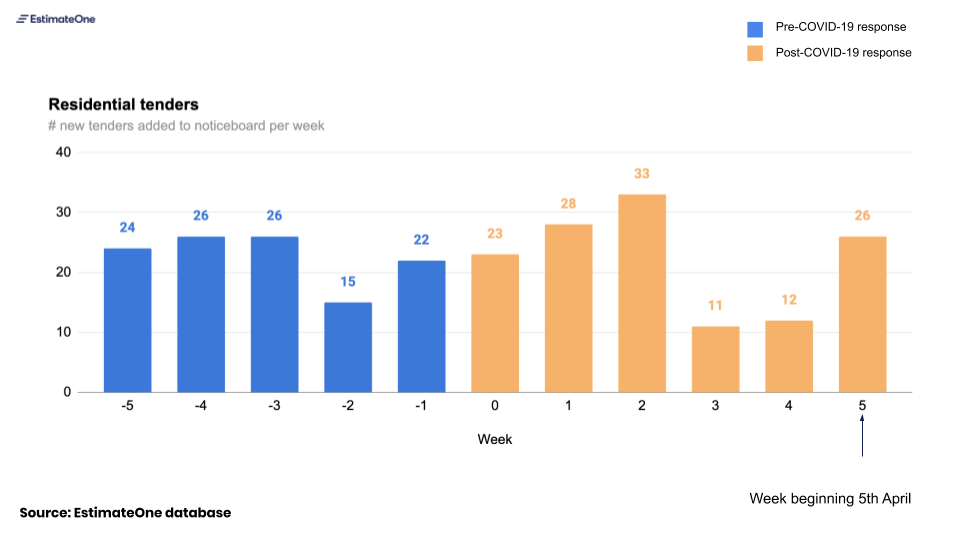

Residential:

Residential tenders saw a similar volume profile to Government and Education – with a sharp drop in ‘Week 3’ and a recovery after that. Unlike Government, the reduction in Residential tender volumes has been most strongly in the higher-value tenders $2m+, with smaller projects less affected.

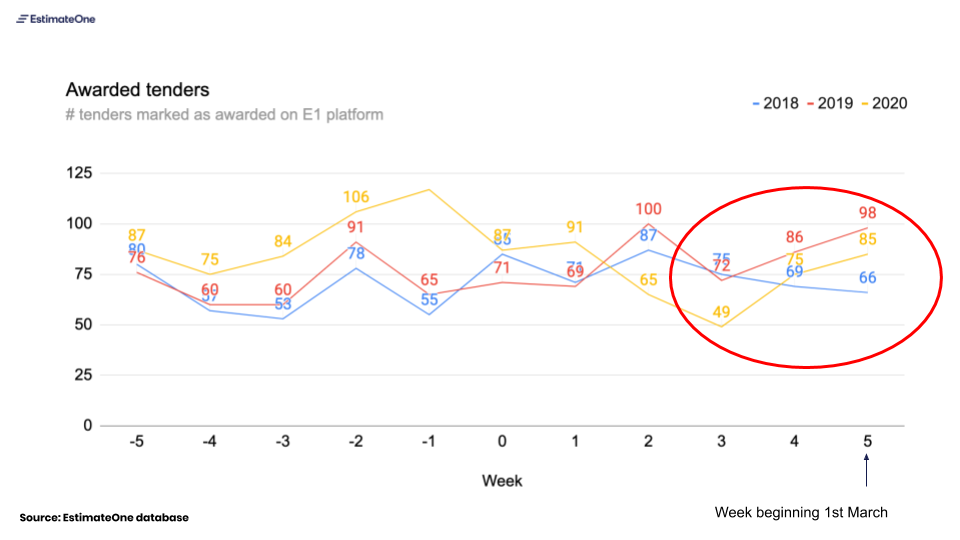

Section 3: Awarded tenders

Commentary

Our last newsletter in Week 3 showed a drop-off in Projects awarded – a measure that regularly tracks between 70 and 100 at this time of year and which had dropped to 49 for the week. These last two weeks have seen a significant pickup in this measure. This supports what we’re hearing from Builder clients: decisions were delayed as the likely impacts of lock-downs for sites and projects were being assessed, and now that there is more certainty projects are continuing to move forward.

What we’re hearing:

Builders have been quick in adopting new collaboration and remote working software to enable their teams to work from home – many of the builders we spoke to expect these new ways of working to remain in place even after the COVID-19 risk has passed.

Although Government clients have shown an inclination to fast-track tenders where possible, this has not (yet) resulted in material volumes of new tenders to offset drop-offs in other categories.

The ‘new’ rules and setups for hygiene and social distancing on site are being a norm, but are difficult to execute well (narrow corridors, lifts and doorways present challenges for distancing).

Shut-down and clean protocols are well established and in use where COVID-19 cases are identified, with minimal disruption to the progress of a project. The impacts to productivity we’re hearing about are more linked to site-measures than to temporary shut-downs.

Subbies, suppliers and builders have all spoken to greater optimism in the past fortnight than in the weeks before. The reality of lockdowns has been less dire than many feared, and the determination to keep sites running (despite the objections of some) seems resolute.

Looking forward

Our view two weeks ago was that stricter lockdowns, like those imposed in New Zealand, were coming. The flattening of the curve challenges this view. If case loads continue to drop, even as authorities work to increase health system capacity, governments may decide Stage 3 restrictions will suffice.

How long these restrictions will be in place depends on which exit strategy authorities select. Australia finds itself in a rare position globally to have a choice between seeking total elimination of the virus (with longer restrictions in the near term), and attempting a controlled infection rate that stabilises the health system (with lesser, but longer restrictions).

Beyond the duration of restrictions, additional uncertainties remain:

Contractual interpretation of Covid impacts for clients, builders, subbies and suppliers remains uncertain for now. Force majeure, repudiation and frustration have all been mooted as protections for stakeholders. Lawyers we’ve spoken with during the week are optimistic that implied duty of good faith will prevail in dealings between parties during these challenging times.

With slumping business confidence ([LINK]) and recession-level unemployment ( [LINK]) both looming, the economic outlook is gloomy, however the depth and duration of this impact for construction industry demain remains uncertain. This impact will depend strongly on the degree to which stimulus efforts focus on creating demand.

We will continue to monitor the impact of the virus and the policy response to it on tendering in our industry in the coming weeks and will share what we find.