During the last fortnight, we have seen further easing of restrictions as ‘normal’ life starts to return. The Government has outlined details of their construction stimulus policy with a heavily means-tested $25k handout to first home buyers and cashed up renovators. While pundits debate the wisdom of such a targeted stimulus package in the residential sector, we retain our focus on the fortunes of commercial construction.

This sendout will focus on how businesses are changing their tendering tactics. It follows on from a newsletter we sent out two weeks ago with data taken from a survey we conducted (you can read it here.)

What we’re seeing

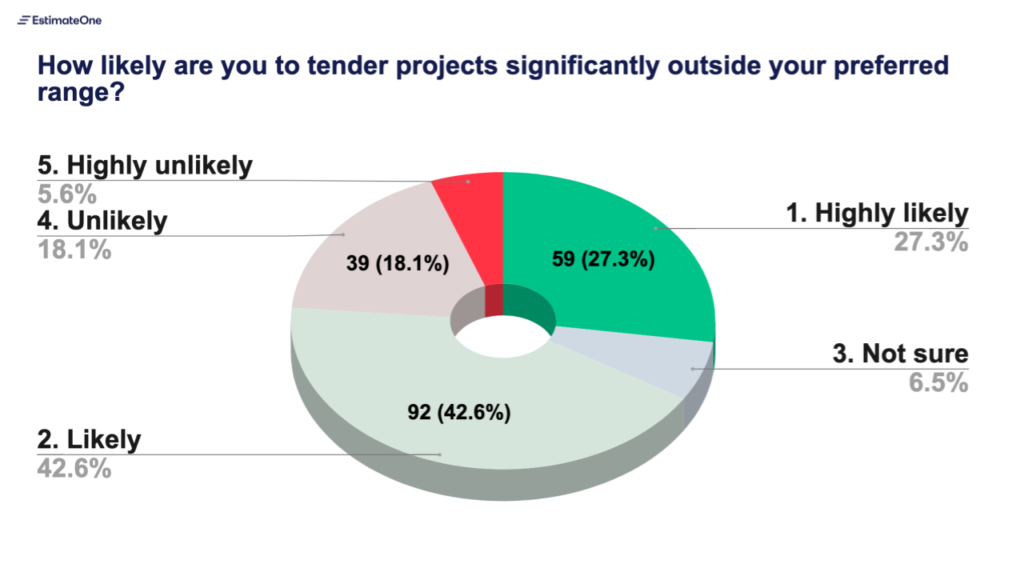

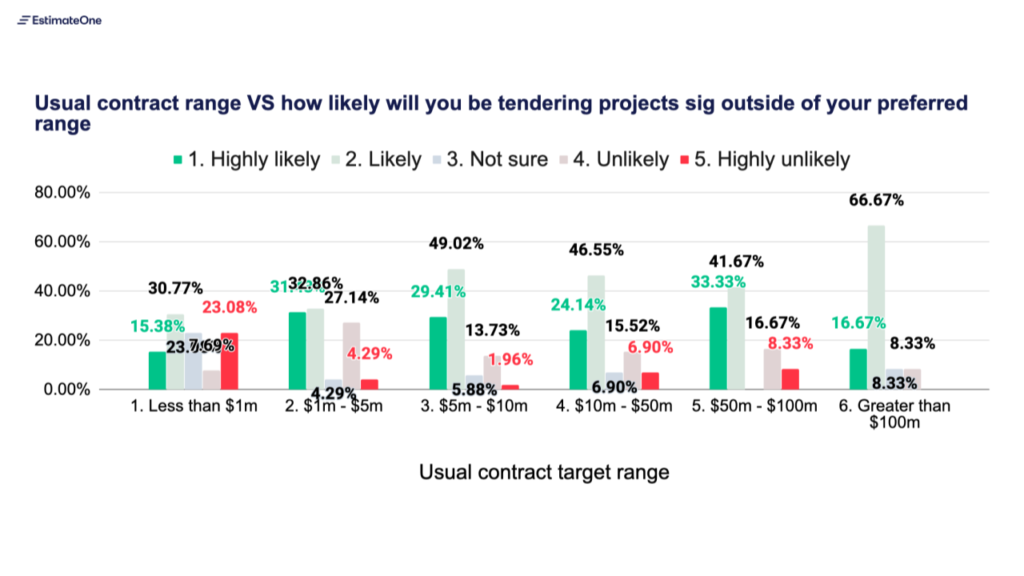

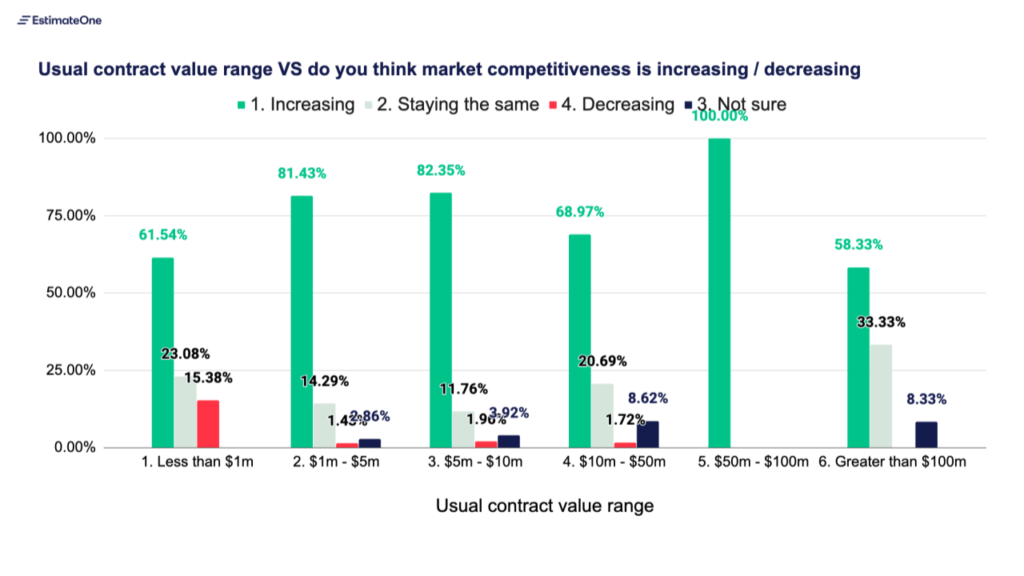

Section 1: Likelihood of tendering projects outside preferred contract value range:

Commentary:

- More than two thirds of our respondents anticipate they will be tendering significantly outside their preferred range in the coming twelve months.

- The higher the preferred contract value range, the more likely the respondent is to anticipate tendering outside of that range.

- Builders are signalling an intent to follow the work: while it isn’t financially desirable for larger builders bid on projects with smaller contract values, it’s a sign that there are less projects available in their target contract range.

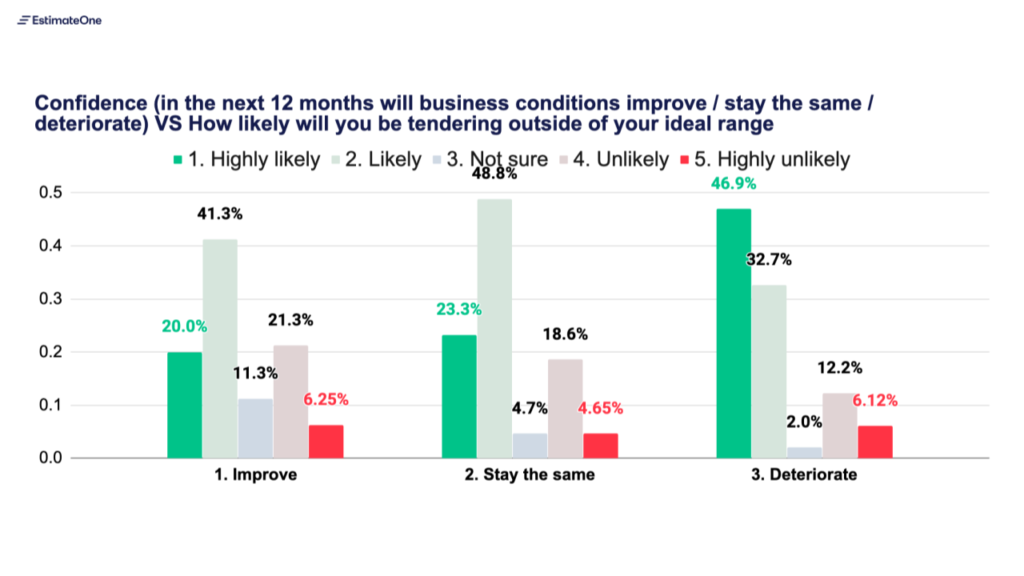

Commentary:

- Businesses who predict market conditions will deteriorate are the most likely to predict they’ll be tendering on jobs significantly outside their contract range.

- These respondents appear to be flagging pro-active changes in the way their business operates. They are signalling a need to be flexible in the face of worsening industry conditions – seeking an extra leg to stand on in a competitive market.

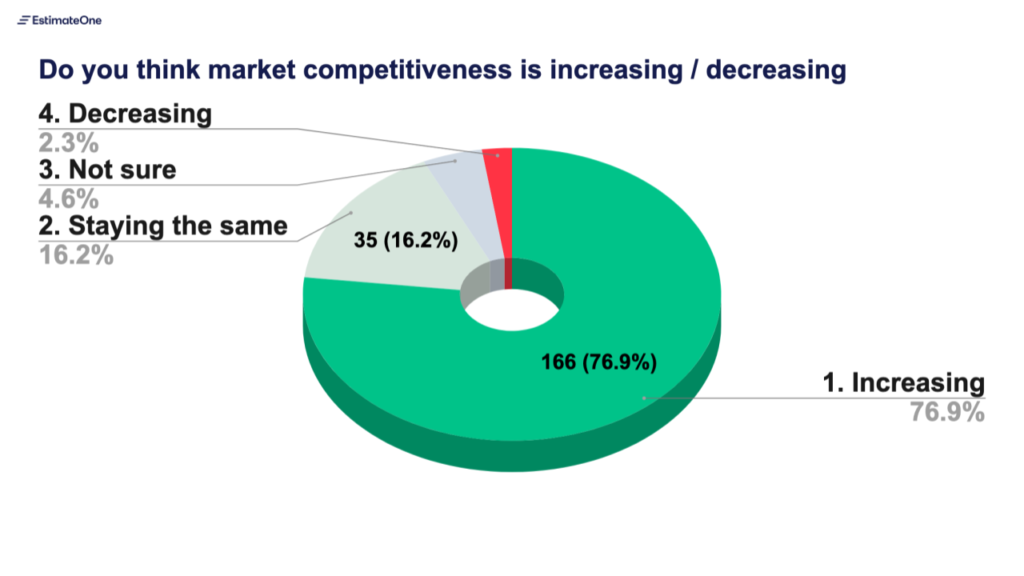

Section 2: Competitive tender panels:

Commentary:

- Like our data suggested in a previous newsletter (link), over three quarters of respondents feel that market competitiveness is increasing.

- Builders who prefer to work with $1 – $10m and $50 – $100m contracts are most likely to note an increase in competition.

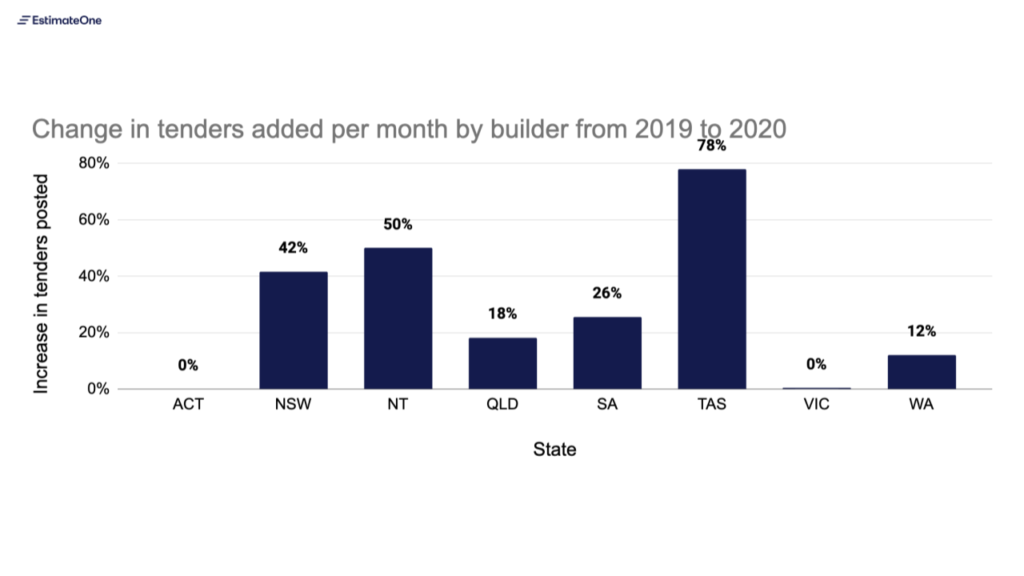

- Below we show a graph showing how builders are increasing the number of projects they are tendering per month. It is likely that the increase of competitiveness in these value ranges is a result of builders upping their tender load in areas where the work currently is.

Commentary:

- This chart shows the change in the number of tenders per month by a given builder, comparing 2020 to 2019. It includes only those builders who tendered in both years (so doesn’t reflect the effect of new entrants or business closures).

- Builders in the majority of states have increased the amount of tenders they bid on per month. With the total number of projects tendered on EstimateOne returning to more normal levels, the increased competitiveness appears to be driven by the market.

What we’re hearing:

Businesses are starting to feel the pinch of competitive tender panels.

- A builder who tenders on contracts under $1m told us that he’s seen an increase in competition on government and residential tender panels. He also told us about an education job he recently tendered on where 30 builders showed up at the site inspection and 20 ended up on the tender panel.

- A survey respondent from Queensland also lamented the more competitive tender panels. They noted that some project panels were now in excess of 10 builders and predicted that the market will remain depressed for the foreseeable future.

- Several builders have told us that selective tender panels have increased from an average of 3-4 builders to 6-7.

More subbie prices are coming in as the fear of underpricing grows.

- One estimator from Queensland told us that he’s seen an increase in subbie quotes coming in – which for him is the canary in the coal mine for market competitiveness.

- Someone had also noted that residential builders are starting to pop up on comercial tender panels. On these jobs they bring their own residential subbies, who are able to quote the work for less.

- “The cost of building hasn’t decreased,” one survey respondent told us. In order to meet the price of the market and get on site, people are quoting much less. The respondent stipulated that the effects of under-pricing will come back to bite the industry in the next six months.

- One builder we spoke to also mentioned that he believes some clients are using the current market conditions to their advantage. He believes clients are looking to lock in lower prices now with no intention to proceed with the build in the near future.

Businesses are becoming much more flexible in order to adapt to the change.

- As a result of increased competitiveness, builders are starting to expand into different sectors in order to lock in any work.

- A builder from New South Wales told us that they’re “seeking any opportunity in any value range to keep people employed”.

- Builders have also let us know how they are diversifying the project sectors they are bidding on. Some builders who would only bid on private tenders have noted they are now bidding on public ones as well.

- Having to work from home is also a reality many builders faced. Some have noted how going forward this will be offered to staff permanently. Adopting new technologies such as zoom was important to ensure collaboration remained in place.

Last week we reached out to everyone with a call to arms to help supply data for our next newsletter. We’re grateful for the more than 200 builders who shared their thoughts within the first 24 hours.

The respondents were not only generous with their time, but also with the level of detail they were willing to go into with their insights. It’s a real joy to see how our industry is banding together to help eachother out in these times.

We’ll share the results over two newsletters, with this sendout focussing on industry confidence and the government’s plan to use construction as a lever to stimulate the economy.

What we’re seeing

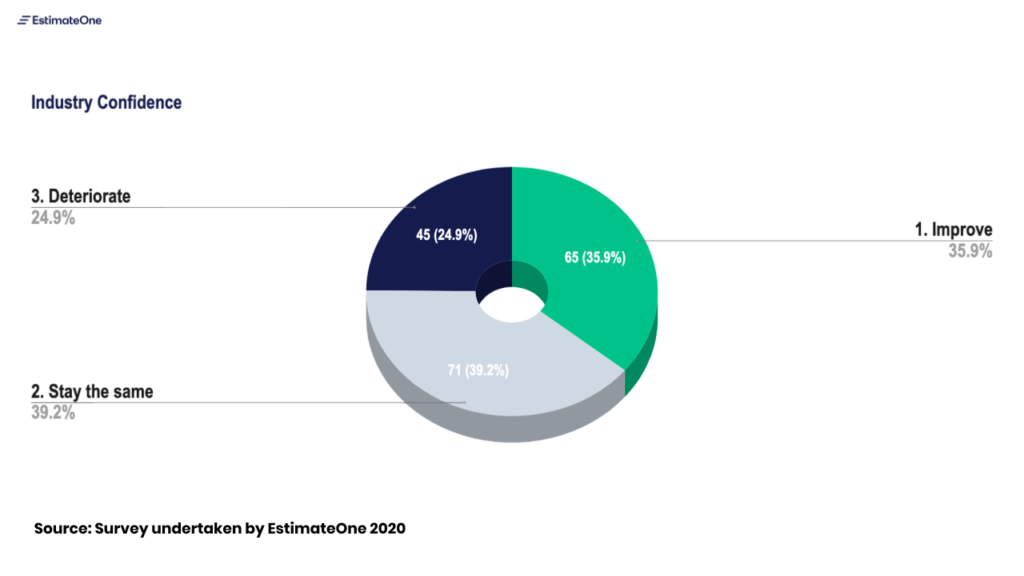

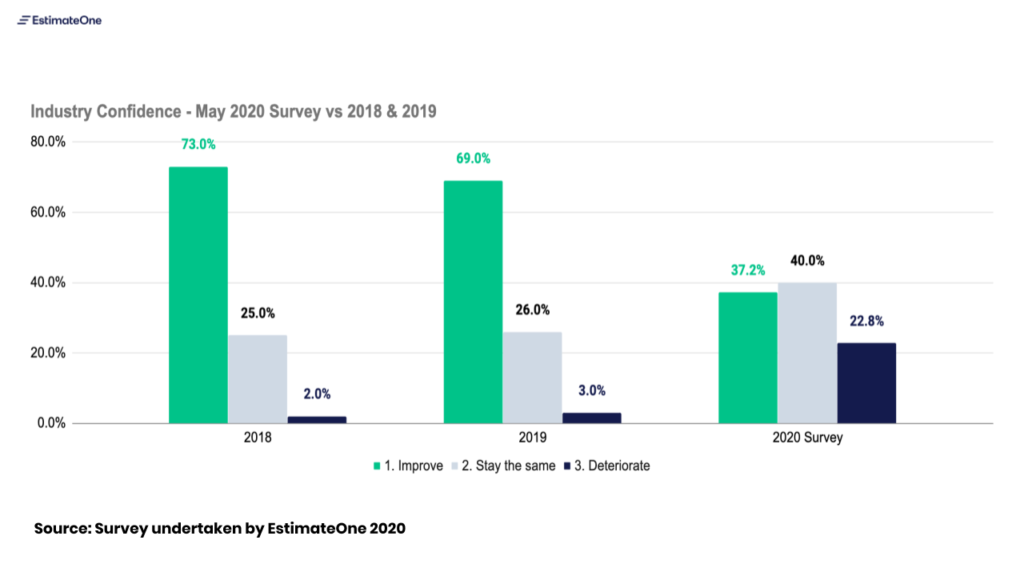

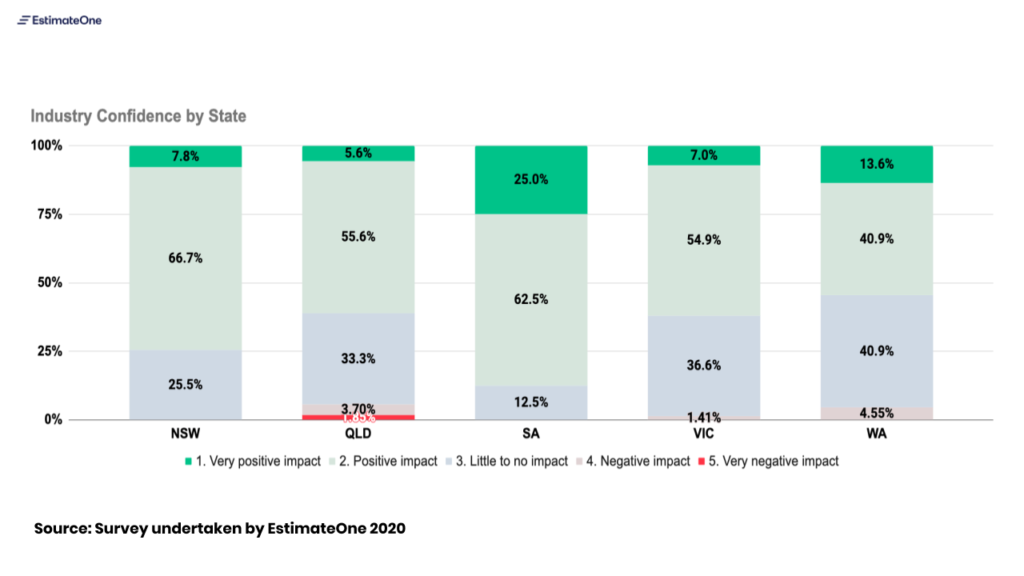

Section 1: Industry Confidence

Question: Over the next 12 months, for your business do you think things will…

As we saw in our analysis of COVID-19 impacts by state and sector, fortunes in the industry are mixed with some bearing the brunt more than others. Confidence is split, though a greater share still expect improvement in conditions compared to those who foresee a deterioration.

We’ve asked this question before as part of our annual industry survey. Here is how it looks when compared to the same question being asked in 2018 and 2019.

Commentary:

- A ten fold increase in people thinking that business conditions will deteriorate in the next 12 months re-enforces the anecdotal evidence we’re hearing; the initial panic has subsided, but much of the industry feels the toughest times are yet to come.

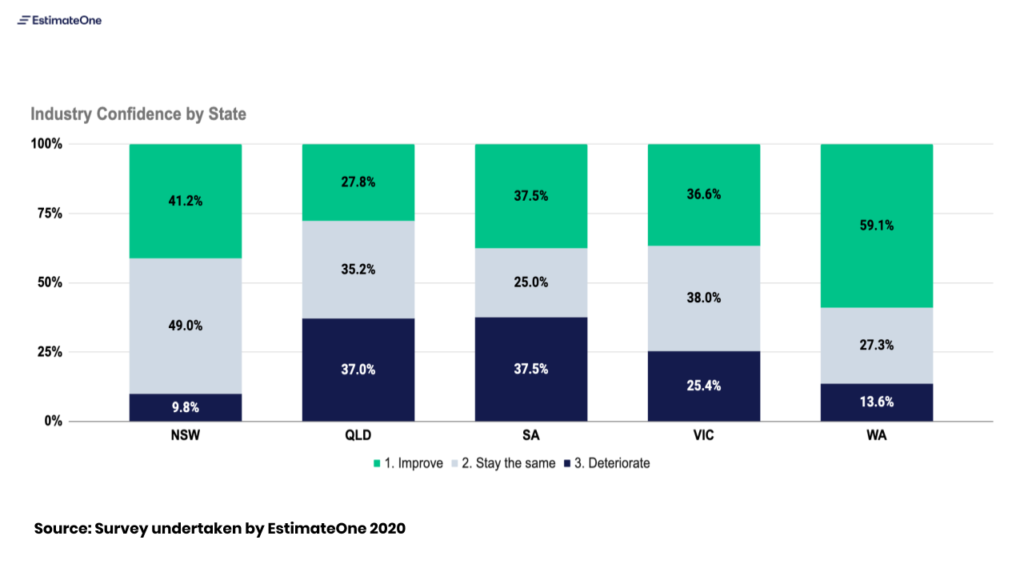

Commentary:

- Industry confidence is down particularly in Queensland. The increase in competition on Queensland panels we showed in our last newsletter could be a contributing factor to this result.

Section 2: Government stimulus:

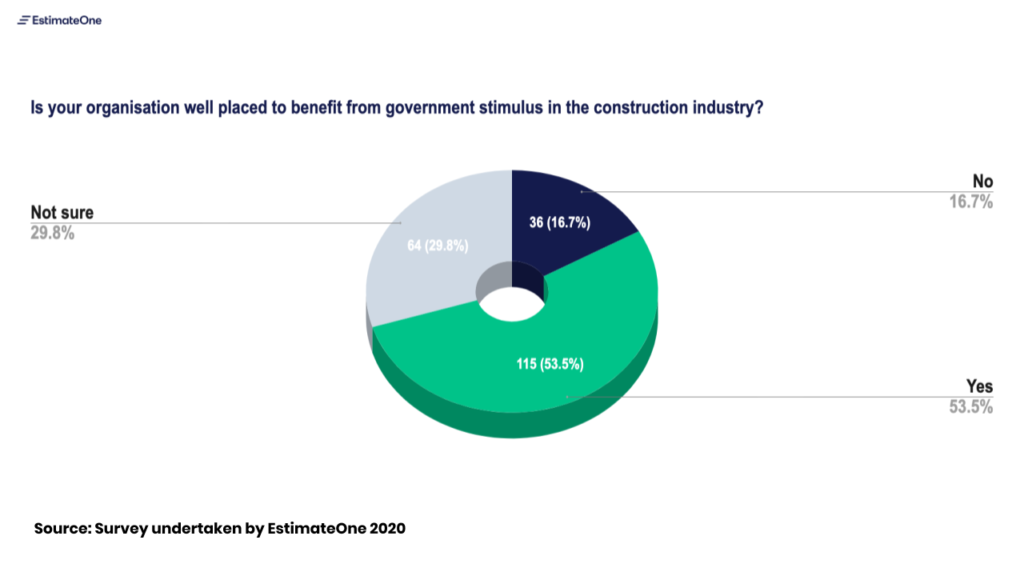

Question: Is your organisation well placed to benefit from government stimulus in the construction industry?

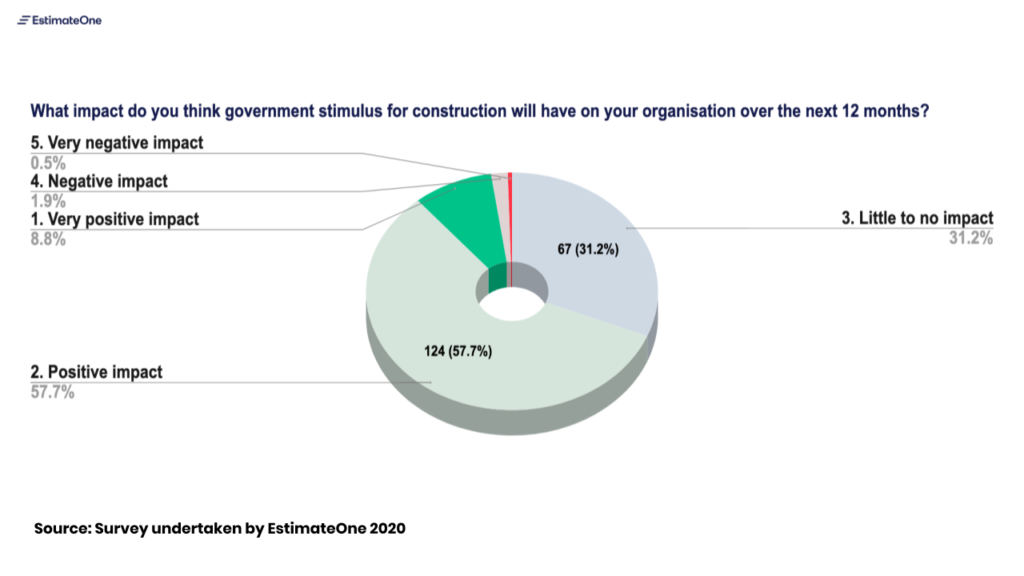

Question: What impact do you think the government stimulus for construction will have on your organisation over the next 12 months?

Commentary:

- A third of those who responded to the survey believe that the stimulus will not effect / have a negative effect on their business.

- Expectations around business confidence were linked to builders’ views on the stimulus; 55% of responders who said at the start of the survey they expect business conditions to deteriorate, believe that the stimulus will have no effect / a negative effect on business.

Commentary:

- Responders in states like NSW (link) and VIC (link) who have started announcing details around planned stimulus policy have the highest confidence that their business will benefit from the packages.

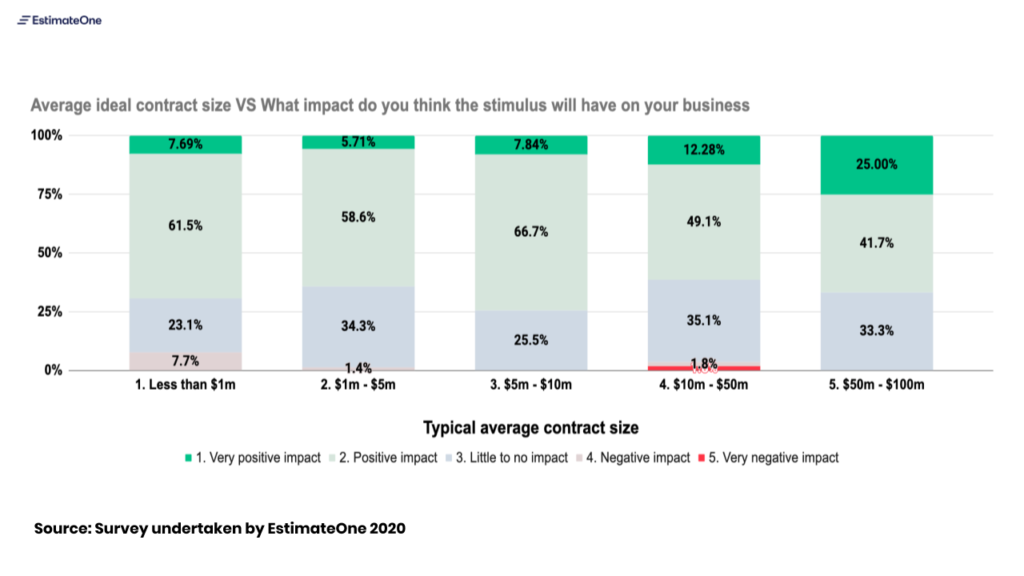

Below is a split of what impact businesses think the stimulus packages will have based by the value of contracts they typically work on.

Commentary:

- We can see that builders who typically work on larger contracts are more confident that they will benefit from the stimulus.

- Conversely, builders who work on smaller contracts are more likely to say that the stimulus will have a negative effect on their business.

What we’re hearing:

As the above data suggests, the government’s plan to use construction as a lever to stimulate the economy has been met with mixed opinions. We gave our responders the option of writing down why they answered the question in a particular way – this has given us the chance to provide deeper insight into the way the industry is feeling.

Many feel the stimulus is geared towards tier one or two builders:

- Many of our respondents wrote to us fearing the lion’s share of the stimulus packages will go to the larger builders.

- One responder claimed that “a lot of projects are in large bundles for the multi-national builders”

- Another responded “The stimulus package will most likely only help the Tier 1 and larger contractors, not the mid tier”

- One responder was hopeful that this stimulus would trickle down to the tier 3 and 4 builders, but expected that to be at least 12 to 18 months away.

- These sentiments could be based on experience, as this is somewhat like what we saw with the Building the Education Revolution (BER) stimulus in the wake of the GFC.

- $16 billion worth of stimulus work was released quickly to the market. The lion’s share of the school packages were awarded to the nation’s largest builders, due in part to the government’s desire to deliver the stimulus to the market quickly via packages of a hundred schools at once.

- In some instances, this resulted in unnecessary levels of additional project management and wastage of funds.

Some feel that the construction stimulus won’t be in the fields they typically operate in.

- One person noted that policy amendments such as the first home buyers scheme will benefit project builders but not those who work on more bespoke / commercial works.

- One noted that they believe the majority of the funds would head to regional areas where their business doesn’t have the subbie contacts required to put in a competitive quote.

- A concern was also shared that these packages will attract their regular subbies to infrastructure works, leaving them at risk in their current tenders / and future awarded tenders

Some worry the stimulus could exacerbate the problem of under-pricing:

- One responder told us: “You still need to win the work, potentially of all the contractors that can complete those projects, there will be a few that will do it for nothing, making it difficult for the majority to win the work.”

- Another responder stipulated that all the stimulus work will have a lot of businesses flocking to it – thus increasing the competitiveness in price required to win it.

Those who are ready / willing to adapt are confident in what the future has to bring.

- A lot of responders wrote that they are confident their business will benefit, as they have gone through all the necessary procedures to complete government work in the past.

- One person wrote “We are restructuring our company to be able to undertake more government work.”

- Quite a few responders also were confident as they had won a lot of education jobs in the past. With education likely to be the lynchpin of many policy announcements, these builders are confident they’ll be able to take advantage of the upcoming packages.

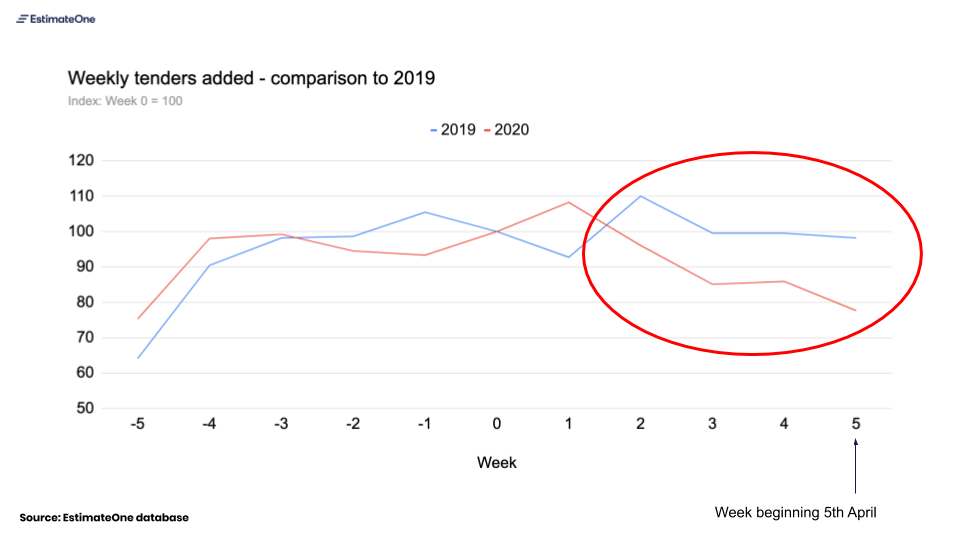

After nearly two months of escalating restrictions, Australia seems to be turning a corner. A new app to complement manual tracing efforts, relaxation of social gathering rules in some states, and an even ‘flatter’ curve have all contributed to a much more optimistic mood in Australia – if not elsewhere in the world.

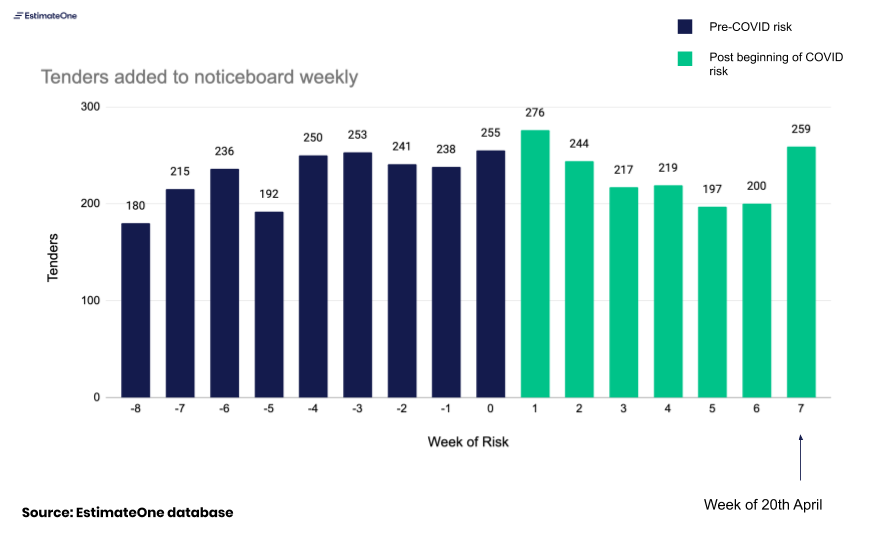

Happily, our data reflect some of this optimism, though the impacts differ by state and by industry. After a slower fortnight that added the Easter long weekend to any COVID impacts, this last week shows a strong pickup to pre-COVID levels of new tenders.

It’s important to caution this result with some of the less optimistic reports we’re hearing, especially about slow-downs in demand at the planning and design stages. The forward view remains uncertain, but this most recent week’s uplift is a welcome start.

Below we share some more detailed observations to help you navigate the impacts to our industry.

What we’re seeing:

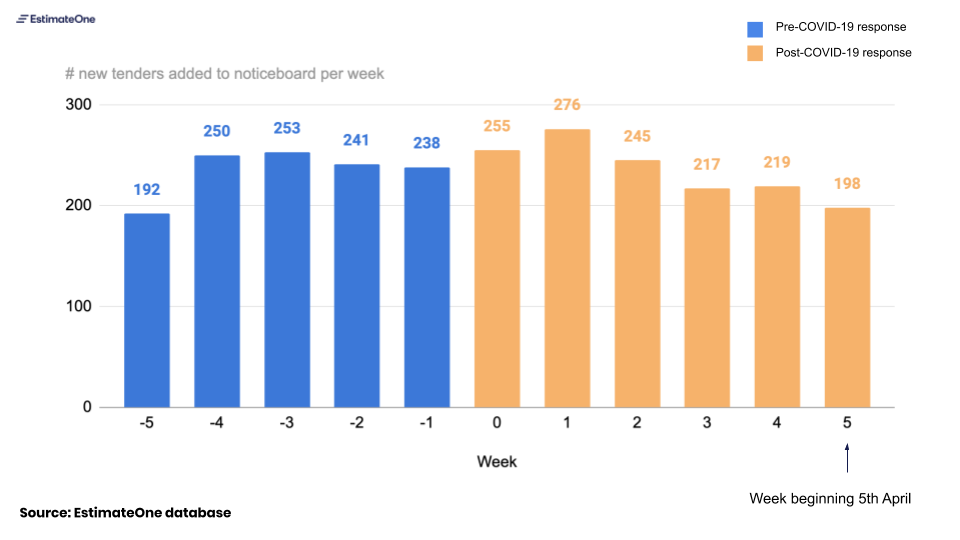

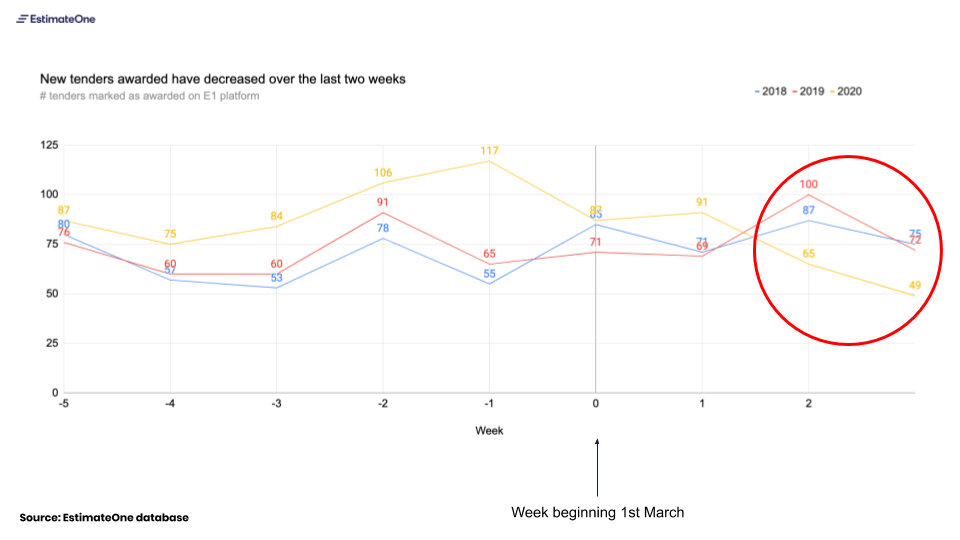

Section 1: Aggregate new tender volumes

Commentary:

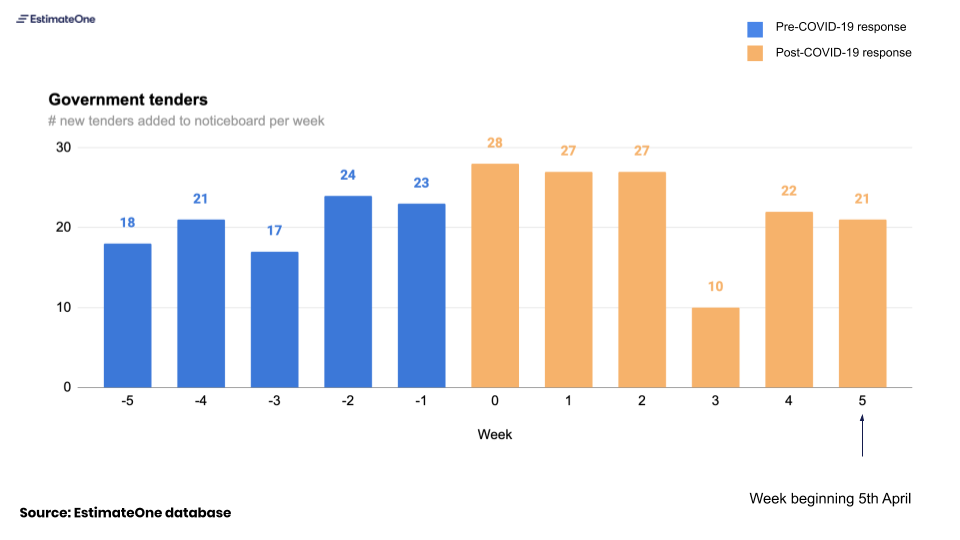

- The overall volume of tenders has increased from 200 in the week of Easter Monday to 259 this last week – back at the level we were seeing before the first impacts of COVID were being felt

- At a category level, Government tenders contributed the most to this increase; there were 49 new tenders from government last week compared to 25 the week prior

- It’s difficult to disentangle the effects of Easter; two four-day weeks might have delayed some tenders going out (leading to a ‘catchup’ effect) in week 7 which makes us hesitant to attribute this to any specific changes in the effects of COVID, but we’ll continue to monitor week by week

Section 2: State by state view

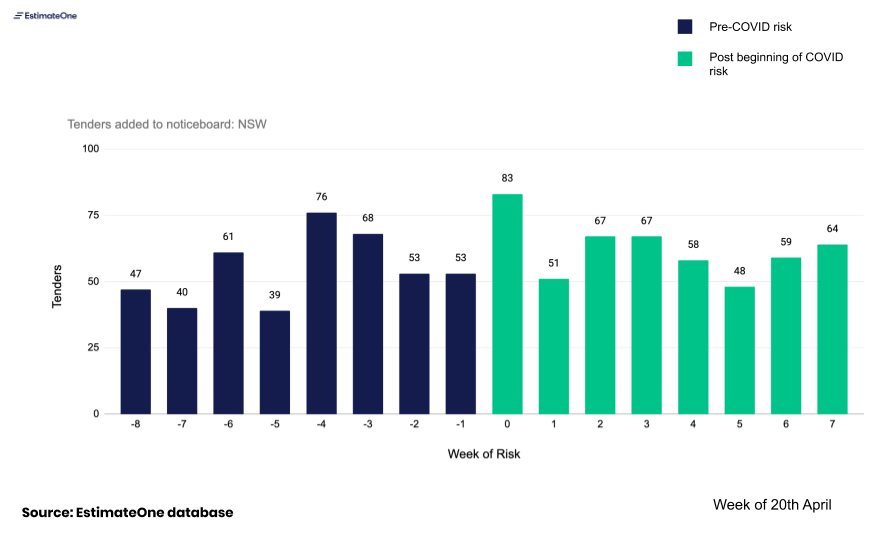

NSW:

Commentary:

- NSW has now seen 60 more tenders in the 8 weeks from the beginning of March than the 8 weeks prior (497 vs 437).

- Between them, Education and Government tenders represent an increase of 52 over the 8 weeks, offsetting falls in Aged Care, Civil and Fit Out tenders over the same period.

- Although builders we spoke to were seeing delays in tender awards and project go-ahead; (consistent with the awarded work data we shared in our previous newsletter), none were experiencing a slow down in new tenders nor had seen evidence of drop-offs in cost planning to date.

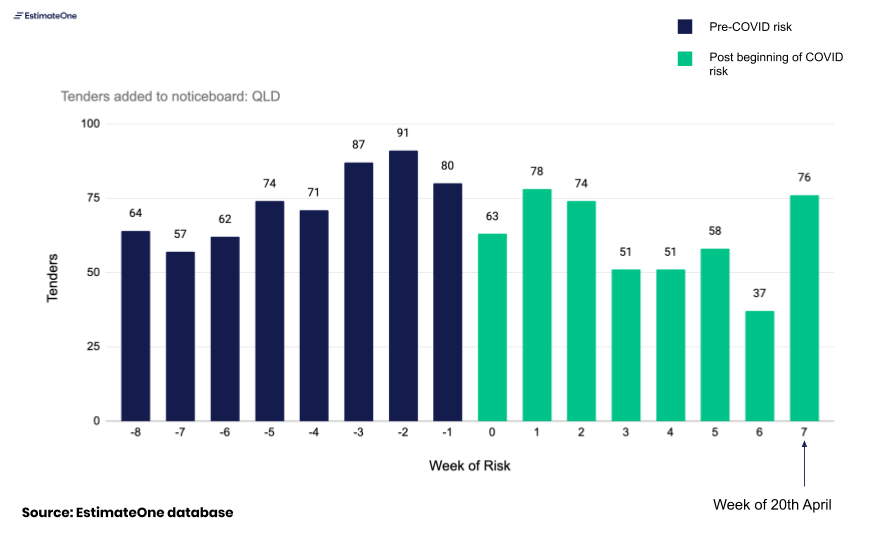

QLD:

Commentary:

- Queensland saw the most obvious ‘bounce’ of any state this last week, getting back to a weekly new tender level in line with the pre-COVID rate, having seen a steady drop-off since Week 0 of the COVID risk.

- This reflected the experience of builders we spoke to; the slow down had been felt but things were beginning to pick up again. Government tenders, in particular Defence and Medical were listed as the most likely to gain pace over the coming weeks, with an expectation that private tenders were more likely to be delayed where clients were in a position to do this.

- Although the increase in tenders happened across all budget ranges, the biggest increase was in the $10m + category (representing roughly a third of tenders in the state) which increased from 8 to 25 week on week.

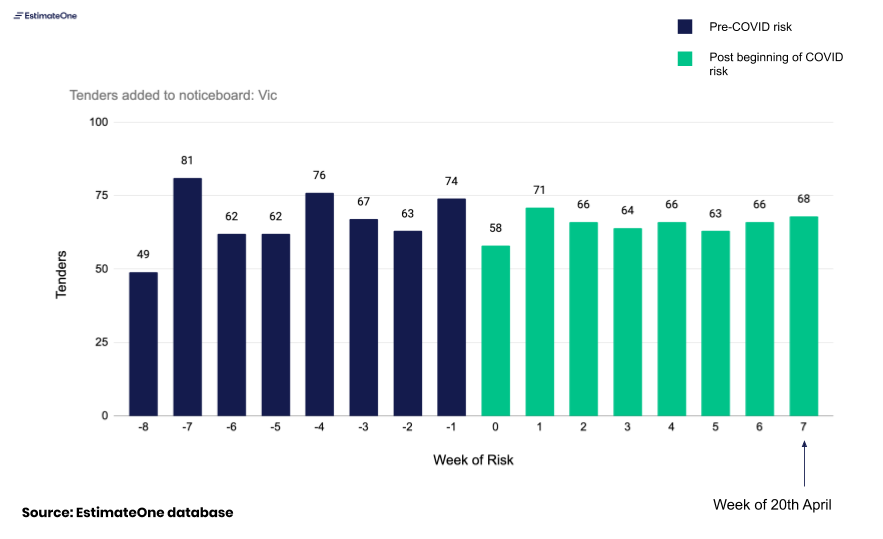

VIC:

- Compared to NSW and especially Queensland Victorian tenders have shown a much steadier trajectory throughout the COVID risk period, although the composition of the state’s tenders has shifted by category. Commercial tenders, which represented roughly a third of tenders between weeks 0 and 3 have dipped since then to under a quarter, with the slack being picked up in part by a small increase in Government tenders.

- Builders we spoke to in VIC told us the state had felt ‘flat’ throughout, though wondered whether this reflected a slower start to 2020 more than any impacts of the COVID risk being felt more recently.

What we’re hearing:

- There is steady support for government funded projects, specifically in corrections, public housing and health. Builders we’ve spoken to have confirmed that this appears set to continue, with confirmations of tender lists for upcoming projects being announced during the last week for new projects.

- Assuming tenders take 3-6 months to prepare and bring to market, some builders are concerned about tenders that should be commencing preparation now, for arrival later in the year

- Both architects and quantity surveyors are reporting a dip in new enquiries for preliminary design and cost plan work, especially associated with new residential projects.

- There is growing concern from several builders around demand for high-density residential projects, especially that which would be classified as “investor stock” which will be more exposed to deteriorating rental market conditions and price expectations.

- Conversely, demand for medium-to-high-density residential projects catering to the owner-occupier market is holding steady.

Looking forward

With restrictions easing rather than tightening, we expect forward conditions for the industry to be impacted more by the demand outlook than by operating conditions.

On the upside, government projects are already representing a greater share of new tenders and we expect this support to continue, with state governments putting together stimulus packages that fast-track and expand already-planned projects. This support will be intended to offset downward pressures in other sectors. challenges to rental demand and projected falls in house prices are likely to threaten at least some sectors of residential demand, while recessionary pressures slow commercial and retail growth.

We’re intending to continue this newsletter as we have updated data. We don’t anticipate sending it more than once per week. If this is not helpful for you, you can unsubscribe by using the button below.

It’s hard to believe the pace with which COVID-19 has spread across the world, and the pace with which authorities and societies have reacted to it. From our vantage point at EstimateOne, although cases and restrictions in Australia have increased since our last newsletter, the initial panic seems to be subsiding.

Efforts across the country to ‘flatten the curve’ appear, for now, to be working. The rate of new cases identified is dropping and health systems remain able to handle the volume of patients presenting with the virus.

The Prime Minister has reaffirmed an intention between his office and the State Premiers’ to keep construction sites running, and this is reflected in continued activity across the industry. Tenders are still flowing, projects are still being awarded and construction sites are continuing to operate; although on all fronts we see the impact of COVID-19.

Below we share some more detailed observations to help you navigate the impacts to our industry.

What we’re seeing:

Section 1: Aggregate new tender volumes

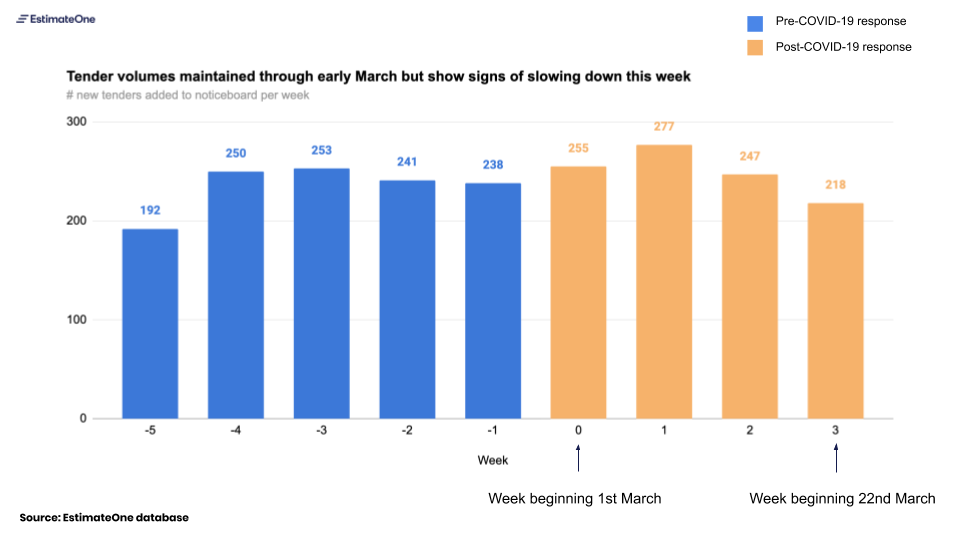

Commentary:

- Tender volumes dropped from around 250 per week to around 220 in Week 3 of the crisis and this most recent week we saw a further drop to 198 – though a shorter week with Good Friday explains this further fall. We expect this coming week, also shorter, to show lower volumes too.

- We have confidence in attributing the March slow down to COVID-19. Last year weekly volumes in March were equal to February numbers, this year they’re ~10-15% down (see chart below)

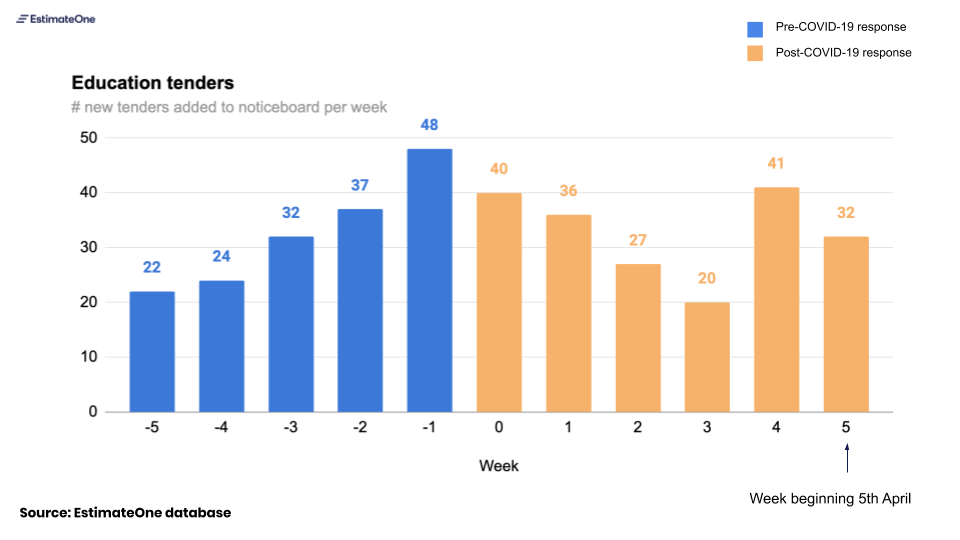

Section 2: Breakdown by sector

Education:

- In the first few weeks of March, education tenders halved from a high point in late February, but the last two weeks have seen an increase. Clients have mentioned education projects in Government pipelines being fast-tracked to tender as a COVID-19 response which may explain this uptick.

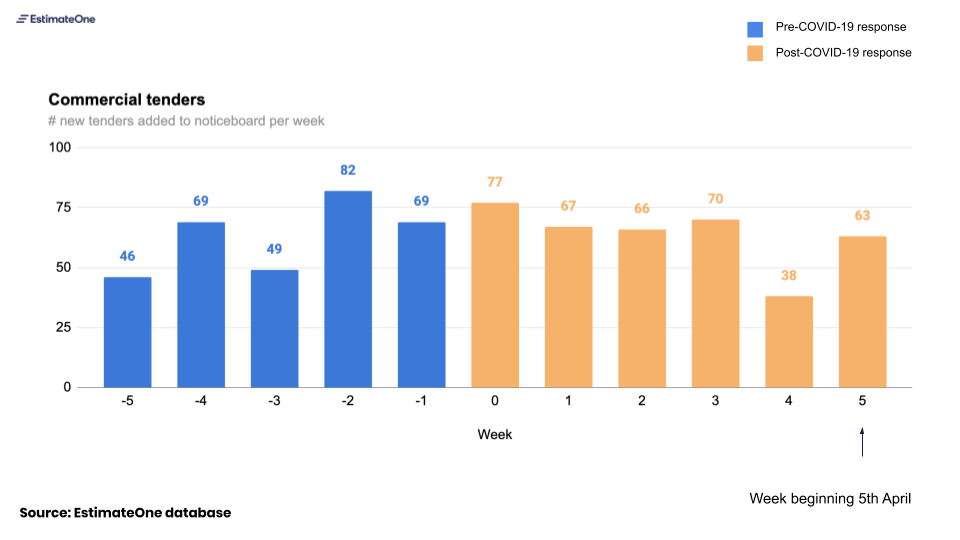

Commercial:

- Commercial had a more moderate drop-off which was concentrated in tenders above $2m (lower price tenders saw a reduction in the early weeks of the crisis but have since rebounded)

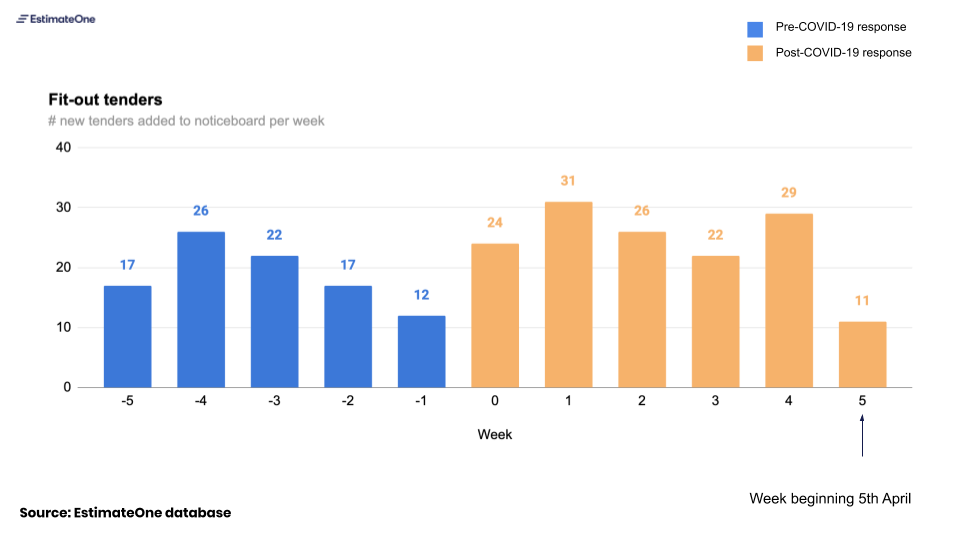

Fitout:

- We anticipated fit-out tenders to be amongst those most affected by the crisis and by the lock downs – but volumes remained higher until this last week where we saw a significant reduction. Our builder clients have suggested that their clients have been seeing opportunities to bring forward smaller projects given their empty offices – this is supported by our data; projects under $2m have actually increased since Week 0. (beginning of March)

Government:

- New government tenders have seen the most significant drop-off amongst sectors (note that this Category excludes tenders categorised to other sectors like Education or Medical which are likely to include Government clients). This drop-off is accounted for largely by a reduction in small tenders $0-$2m, with tender volumes $2m+ holding steady through February and March.

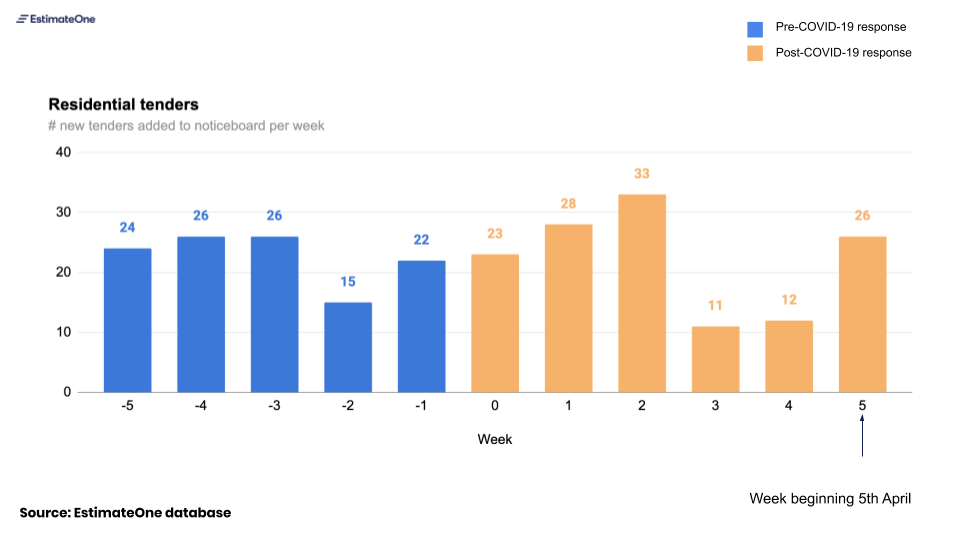

Residential:

- Residential tenders saw a similar volume profile to Government and Education – with a sharp drop in ‘Week 3’ and a recovery after that. Unlike Government, the reduction in Residential tender volumes has been most strongly in the higher-value tenders $2m+, with smaller projects less affected.

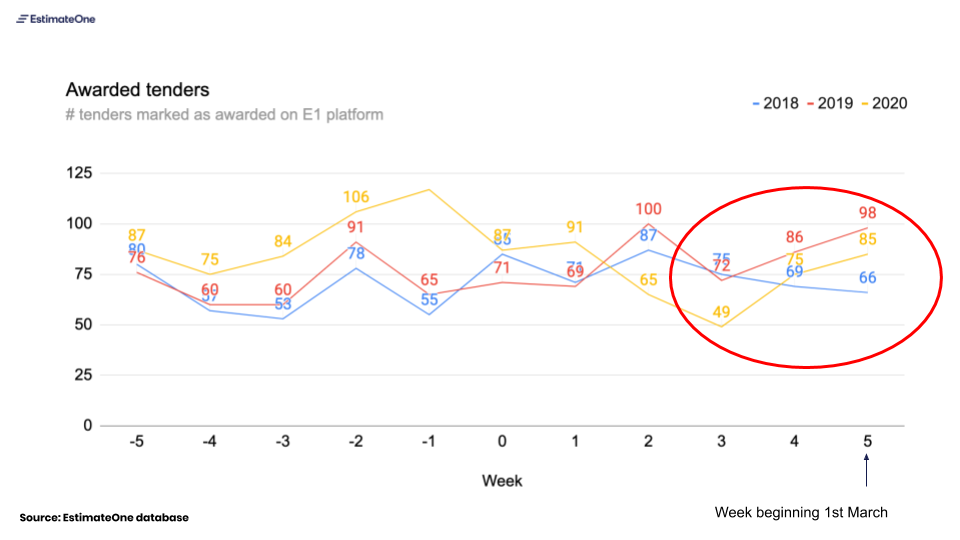

Section 3: Awarded tenders

Commentary

- Our last newsletter in Week 3 showed a drop-off in Projects awarded – a measure that regularly tracks between 70 and 100 at this time of year and which had dropped to 49 for the week. These last two weeks have seen a significant pickup in this measure. This supports what we’re hearing from Builder clients: decisions were delayed as the likely impacts of lock-downs for sites and projects were being assessed, and now that there is more certainty projects are continuing to move forward.

What we’re hearing:

- Builders have been quick in adopting new collaboration and remote working software to enable their teams to work from home – many of the builders we spoke to expect these new ways of working to remain in place even after the COVID-19 risk has passed.

- Although Government clients have shown an inclination to fast-track tenders where possible, this has not (yet) resulted in material volumes of new tenders to offset drop-offs in other categories.

- The ‘new’ rules and setups for hygiene and social distancing on site are being a norm, but are difficult to execute well (narrow corridors, lifts and doorways present challenges for distancing).

- Shut-down and clean protocols are well established and in use where COVID-19 cases are identified, with minimal disruption to the progress of a project. The impacts to productivity we’re hearing about are more linked to site-measures than to temporary shut-downs.

- Subbies, suppliers and builders have all spoken to greater optimism in the past fortnight than in the weeks before. The reality of lockdowns has been less dire than many feared, and the determination to keep sites running (despite the objections of some) seems resolute.

Looking forward

Our view two weeks ago was that stricter lockdowns, like those imposed in New Zealand, were coming. The flattening of the curve challenges this view. If case loads continue to drop, even as authorities work to increase health system capacity, governments may decide Stage 3 restrictions will suffice.

How long these restrictions will be in place depends on which exit strategy authorities select. Australia finds itself in a rare position globally to have a choice between seeking total elimination of the virus (with longer restrictions in the near term), and attempting a controlled infection rate that stabilises the health system (with lesser, but longer restrictions).

Beyond the duration of restrictions, additional uncertainties remain:

- Contractual interpretation of Covid impacts for clients, builders, subbies and suppliers remains uncertain for now. Force majeure, repudiation and frustration have all been mooted as protections for stakeholders. Lawyers we’ve spoken with during the week are optimistic that implied duty of good faith will prevail in dealings between parties during these challenging times.

- With slumping business confidence ([LINK]) and recession-level unemployment ( [LINK]) both looming, the economic outlook is gloomy, however the depth and duration of this impact for construction industry demain remains uncertain. This impact will depend strongly on the degree to which stimulus efforts focus on creating demand.

We will continue to monitor the impact of the virus and the policy response to it on tendering in our industry in the coming weeks and will share what we find.

Over the past few weeks we have been talking at EstimateOne about how we can support our industry while it grapples with the challenge of COVID-19.

In the interest of sharing information to help everyone make better decisions, here are some observations made from our own platform. With more than 400 active head contractors and more than 40,000 active subbies and suppliers using EstimateOne, we believe we are well placed to provide analysis to support the industry as we all try to understand what’s happening right now, and what we should do next.

What we’re seeing:

Chart 1: New tender volumes

Commentary:

- We compared the new tenders added to our notice board by builders from before the crisis to after. We treat March 1st as the ‘beginning’ of the crisis (the 29th of February marked the first significant policy response from the Federal government with the implementation of compulsory self-isolation for returnees from several other countries).

- For the first three weeks volumes tracked ‘BAU’. Last week was the first week we’ve seen a slow down in tenders with 218 tenders compared to an average of 260 in the week previous. Typically the middle of the week is busiest for new tenders, with between 40-60 added to the noticeboard each day; on Wednesday and Thursday this week we had only 22 and 27 respectively (though this picked up on Friday).

Chart 2: Awarded tenders

Commentary

- The number of projects awarded by week is often a ‘noisy’ number for us (it depends, amongst other things, on builders reporting their awards on the platform), but the reduction over the past two weeks supports what we’ve been hearing from our builders – that clients are deferring their award decisions where possible.

Chart 3: Subcontractor delinquency

Commentary:

- Cash flow for all parties in the industry is a concern through this period. One indicator we track is the decline rate for credit card transactions (for our noticeboard subscriptions). This rate has increased only slightly from its usual 5% to 5.6% over the past week.

What we’re hearing:

- As of the weekend there is still an intention to keep sites running for active projects. Construction sites are deemed ‘necessary activity’ under the national guidelines, and we haven’t heard (yet) of site shutdowns.

- Tendering is still active and volumes have been ‘normal’ throughout most of March (this corresponds with data shown above).

- Builders are adapting to social distancing rules quickly where this is possible: many have implemented blanket working-from home policies or are working with rotating in-office shifts (dividing the business into teams who rotate in and out of the office). On-site options are more challenging, but builders are implementing new practices for hygiene and distancing on site, creating more space for amenities. Staggered working hours are being considered on some sites.

- Early impacts of COVID-19 are being seen in Head Contractor awards: clients are deferring award decisions in the face of uncertainty in their own businesses and the economic environment (this is reflected in our data).

- Business Development activity has slowed right down, a combination of remote work plus a desire to defer decisions whilst the outlook remains uncertain.

- Departments of Health are paying additional funds to accelerate progress on live jobs, in particular those which yield additional ICU beds.

Our view of what’s coming

- It’s likely further lockdown restrictions will be put in place, especially if States decide to move on their own. Stage-3 restrictions in Victoria (as an example), adopted after the National Cabinet announcement on Sunday, still permit construction activity to continue, but Premier Andrews has signalled a willingness to move ahead of National guidelines.

- Rules for sites will become more, not less, restrictive in the near term. NZ-style restrictions are likely, where “essential” construction activity is that which is related to the building of essential services and/or human health.

- New fit-out tenders are likely to see a material drop-off as clients defer decisions on new office moves/refurbishments whilst their staff work remotely.

There will be concerted efforts to develop test kits for rapid detections of antibodies, allowing people who have developed an immunity to the virus back on site. UK researchers should announce material progress this week. Link

We’re intending to continue this newsletter as we have updated data. We don’t anticipate sending it more than once per week. If this is not helpful for you, you can unsubscribe by using the unsubscribe button below.

This is a difficult time for everyone. We all have a part to play in supporting each other and our industry through this challenge.

Our commitment is to continue to provide insights and observations as we see them over the coming months, in the hope that they may help you make the best decisions for your business. If you have questions you think we can help you answer – we’re here to help.

Our thoughts are with you, your organisations and your families.

Cheers,

Mike

Michael Ashcroft

Founder, EstimateOne